Magazines

News Journal: Number 29, October 26, 2010: American People’s No Confidence Voting Wave Wipes Out Democrats–It’s The Economy Stupid!–Videos

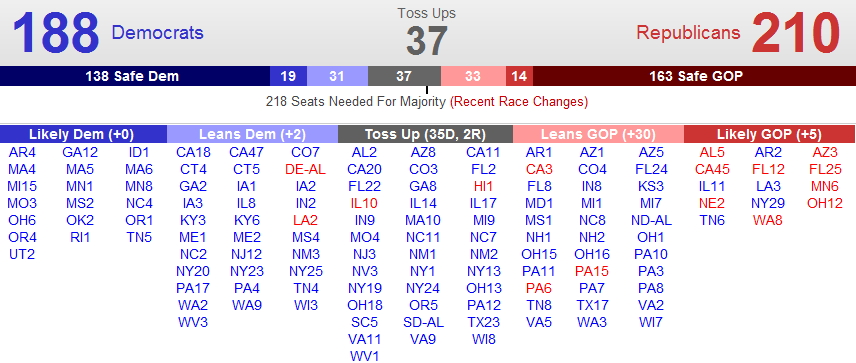

Republican Governors 35

Republican Senators 51

Republican Representatives 255

The Republicans will pickup a net total of 77 seats in House of Representatives for a total of 255.

The Republicans will also pickup a net total of 10 seats in the Senate for a total of 51 seats.

The American people want to stop the massive Government spending, deficits and bailouts and rising National debt of the Obama Administration.

Stop Spending Our Future – The Crisis

Issue number 1 is jobs and the economy with nearly thirty million Americans looking for a full-time job and continuing high rates of unemployment.

Issue number 2 is massive Federal Government spending, deficits, bailouts and a rising National debt.

The National Debt Road Trip

The Trillion $$$ Dollar U.S. Economic Deficit Caused By Our Government

U.S. Debt Clock

Issue number 3 is Obamacare– the American people want it repealed as soon as possible and no money bills or appropriations to fund Obamacare.

Fight Obamacare Texas

Issue number 4 is illegal immigration–the American people want it stopped by immigration law enforcement and a completed border fence that is heavily patrolled.

What Are True Costs And Benefits Of Illegal Immigration?

Stop Illegal Immigration

The American people expect the Republican Party to balance the Federal Budget by significantly reducing Government spending and permanently closing Federal Departments including Agriculture, Commerce, Education, Energy, Health and Human Services, Housing and Urban Development, Interior, Labor, and Transportation.

The number of Federal employees should be cut from over 2,000,000 to less than 1,000,000.

3 Reasons Public Sector Employees are Killing the Economy

The American people expect the Republican Party to make the Bush tax cuts permanent for all taxpayers and pass the FairTax–it is time!

The American people expect the Republican Party to make the Bush tax cuts permanent for all taxpayers and pass the FairTax–it is time!

The FairTax: It’s Time

Should the Republican Party fail to balance the budget and cut the size and scope of the Federal Government by permanently shutting down the above departments, these Republicans will be wiped out by the 2012 wave of tea party patriots.

Background Articles and Videos

Editor in Chief Insights: Obama’s Job Approval Trajectory

President Obama Heads into Midterms at Lowest Approval Rating of Presidency

Two-thirds of Americans believe country going off on the wrong track

“…Currently, two-thirds of Americans (67%) have a negative opinion of the job President Obama is doing while just over one-third (37%) have a positive opinion. This continues the president’s downward trend and he is now at the lowest job approval rating of his presidency.

These are some of the results of The Harris Poll of 3,084 adults surveyed online between October 11 and 18, 2010 by Harris Interactive.

It’s perhaps not surprising that nine in ten Republicans (90%) and Conservatives (89%) give the job the president is doing negative ratings. What may be surprising is that one-third of Democrats (34%) and Liberals (33%) also give him negative ratings, as do seven in ten Independents (70%) and six in ten Moderates (60%).

Americans who give the president the highest positive ratings are those with a post-graduate education (48%), a college education (47%), and those living in the West (42%). On the other end of the spectrum, almost three-quarters of those with a high school education or less (72%) and two-thirds of Midwesterners (66%) and Southerners (66%) give the President negative marks on his overall job.

While the president is at a low point, there is a political body with ratings much lower than his. Just one in ten Americans (11%) give Congress positive ratings on the job they are doing while nine in ten (89%) give them negative marks. While Congress may be under Democratic control, even four in five Democrats (81%) give them negative ratings.

Part of this negativity may have to do with the way Americans believe the country as a whole is going. Just one-third of U.S. adults (34%) say the country is going in the right direction while two-thirds (66%) say it is going off on the wrong track. While not close to the low it was before the 2008 election (11% said things were going in the right direction), this is one of the lower points of this year. …”

http://www.harrisinteractive.com/Hi_assets/TopHitPageNews.html

Rasmussen Reports

Trust on Issues

Voters Trust Republicans More on Eight of 10 Key Issues

“…Voters now trust Democrats over Republicans in only two areas – government ethics and corruption by a 41% to 36% margin and education where Democrats have a slight 42% to 40% edge.

The economy continues to be the most important issue on voters’ minds this election, and 49% place their trust in Republicans to handle this issue. Thirty-nine percent (39%) trust Democrats more. These findings show little change from early June 2009.

On the issue of health care, which voters place second on the list of important issues, Republicans hold a modest 47% to 40% advantage. Democrats were trusted more on this issue until the debate over a proposed national health care bill began to heat up in early September of last year.

Most voters continue to favor repeal of the national health care law, but the number of voters who expect the law to increase the deficit has fallen to the lowest point since its passage by Congress in March.

(Want a free daily e-mail update? If it’s in the news, it’s in our polls). Rasmussen Reports updates are also available on Twitter or Facebook.

Two surveys of 1,000 Likely U.S. Voters each were conducted October 12-13 and October 14-15, 2010 by Rasmussen Reports. The margin of sampling error is +/- 3 percentage points with a 95% level of confidence. Field work for all Rasmussen Reports surveys is conducted by Pulse Opinion Research, LLC. See methodology.

Government ethics and corruption rate number three in terms of overall importance, but voters have been narrowly divided for the past several months over which party to trust more on this issue. Democrats have held small leads since February.

As for education, both parties have held very modest leads on the issue at different times for months now.

Forty-eight percent (48%) of voters nationwide place their trust in the hands of Republicans when it comes to the issue of taxes. Thirty-nine percent (39%) would rather the Democrats handle this issue. The GOP has held a solid lead over Democrats on this issue since early July 2009.

But most voters believe that Democrats in Congress want to raise taxes and spending, while Republicans in Congress want to cut taxes and spending.

When it comes to immigration, 45% trust Republicans, while 33% trust the Democrats more. The gap between the two parties has widened since the beginning of January as the debate over the immigration law in Arizona intensified. At the beginning of the year, voters were essentially evenly divided on which party to trust.

Voters feel more strongly than ever that the federal government is encouraging illegal immigration and that states like Arizona have the answer to the problem, but the Obama administration is challenging the Arizona law in federal court.

Republicans continue to be trusted more on national security issues and the war on terror, with 49% of voters trusting the GOP versus 39% who trust the Democrats more. When it comes the war in Afghanistan, Republicans hold a six-point advantage, 42% to 36%.

Similarly, voters trust Republicans more than Democrats to handle the war in Iraq, 43% to 37%. …”

http://www.rasmussenreports.com/public_content/politics/mood_of_america/trust_on_issues

Historical Federal Workforce Tables

Executive Branch Civilian Employment Since 1940

(end-of-fiscal-year count, excluding Postal Service, in thousands)

| Fiscal Year | Total Executive Branch | Department of Defense | Civilian Agencies | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Total | Agriculture | HHS, Education, Social Sec. 1 | Homeland Security | Interior | Justice | Transportation | Treasury | Veterans | Other | |||

| 1940 | 699 | 256 | 443 | 98 | 9 | 18 | 46 | 11 | … | 45 | 40 | 176 |

| 1941 | 1,081 | 556 | 525 | 91 | 10 | 20 | 50 | 15 | … | 52 | 43 | 244 |

| 1942 | 1,934 | 1,291 | 643 | 95 | 11 | 20 | 49 | 22 | … | 55 | 44 | 348 |

| 1943 | 2,935 | 2,200 | 735 | 109 | 11 | 21 | 43 | 23 | … | 69 | 53 | 406 |

| 1944 | 2,930 | 2,246 | 683 | 78 | 11 | 21 | 42 | 21 | … | 81 | 51 | 378 |

| 1945 | 3,370 | 2,635 | 736 | 82 | 11 | 20 | 45 | 19 | … | 84 | 65 | 409 |

| 1946 | 2,212 | 1,416 | 795 | 97 | 12 | 20 | 51 | 17 | … | 95 | 169 | 335 |

| 1947 | 1,637 | 859 | 777 | 88 | 12 | 20 | 53 | 17 | … | 82 | 217 | 288 |

| 1948 | 1,569 | 871 | 698 | 82 | 13 | 18 | 57 | 20 | … | 79 | 196 | 233 |

| 1949 | 1,573 | 880 | 694 | 87 | 12 | 19 | 59 | 19 | … | 77 | 195 | 226 |

| 1950 | 1,439 | 753 | 686 | 84 | 13 | 20 | 66 | 20 | … | 76 | 188 | 219 |

| 1951 | 1,974 | 1,235 | 738 | 81 | 16 | 21 | 65 | 25 | … | 79 | 183 | 269 |

| 1952 | 2,066 | 1,337 | 729 | 79 | 15 | 22 | 61 | 25 | … | 75 | 175 | 278 |

| 1953 | 2,026 | 1,332 | 694 | 78 | 35 | 22 | 59 | 23 | … | 71 | 178 | 226 |

| 1954 | 1,875 | 1,209 | 666 | 76 | 35 | 21 | 56 | 24 | … | 67 | 179 | 207 |

| 1955 | 1,860 | 1,187 | 673 | 86 | 40 | 21 | 54 | 24 | … | 65 | 178 | 206 |

| 1956 | 1,864 | 1,180 | 684 | 89 | 46 | 20 | 53 | 24 | … | 64 | 177 | 210 |

| 1957 | 1,869 | 1,161 | 708 | 96 | 53 | 20 | 55 | 24 | … | 65 | 174 | 222 |

| 1958 | 1,817 | 1,097 | 720 | 101 | 55 | 20 | 56 | 24 | … | 64 | 172 | 227 |

| 1959 | 1,805 | 1,078 | 727 | 97 | 59 | 20 | 55 | 23 | … | 63 | 171 | 238 |

| 1960 | 1,808 | 1,047 | 761 | 99 | 62 | 21 | 56 | 24 | … | 62 | 172 | 265 |

| 1961 | 1,825 | 1,042 | 782 | 103 | 70 | 20 | 59 | 25 | … | 67 | 175 | 265 |

| 1962 | 1,896 | 1,070 | 827 | 111 | 77 | 20 | 63 | 25 | … | 69 | 177 | 284 |

| 1963 | 1,911 | 1,050 | 861 | 116 | 81 | 21 | 73 | 25 | … | 73 | 173 | 300 |

| 1964 | 1,884 | 1,030 | 855 | 108 | 83 | 21 | 70 | 26 | … | 72 | 172 | 302 |

| 1965 | 1,901 | 1,034 | 867 | 113 | 87 | 21 | 71 | 27 | … | 74 | 167 | 307 |

| 1966 | 2,051 | 1,138 | 913 | 119 | 100 | 21 | 75 | 27 | … | 76 | 170 | 324 |

| 1967 | 2,251 | 1,303 | 949 | 122 | 106 | 24 | 77 | 27 | 52 | 79 | 173 | 289 |

| 1968 | 2,289 | 1,317 | 972 | 123 | 117 | 23 | 78 | 29 | 56 | 79 | 176 | 292 |

| 1969 | 2,301 | 1,342 | 960 | 125 | 113 | 21 | 75 | 30 | 58 | 79 | 175 | 283 |

| 1970 | 2,203 | 1,219 | 983 | 118 | 112 | 23 | 75 | 33 | 62 | 84 | 169 | 308 |

| 1971 | 2,144 | 1,154 | 989 | 120 | 115 | 25 | 72 | 38 | 66 | 86 | 180 | 288 |

| 1972 | 2,117 | 1,108 | 1,009 | 118 | 114 | 29 | 72 | 40 | 65 | 90 | 184 | 295 |

| 1973 | 2,083 | 1,053 | 1,030 | 113 | 128 | 29 | 74 | 43 | 66 | 90 | 198 | 289 |

| 1974 | 2,140 | 1,070 | 1,070 | 116 | 142 | 30 | 77 | 46 | 68 | 97 | 202 | 292 |

| 1975 | 2,149 | 1,042 | 1,107 | 121 | 147 | 31 | 80 | 47 | 69 | 101 | 213 | 297 |

| 1976 | 2,157 | 1,010 | 1,147 | 128 | 155 | 32 | 82 | 48 | 71 | 105 | 222 | 303 |

| 1977 | 2,182 | 1,009 | 1,173 | 132 | 159 | 32 | 87 | 48 | 70 | 107 | 224 | 313 |

| 1978 | 2,224 | 1,000 | 1,225 | 138 | 161 | 37 | 84 | 49 | 70 | 110 | 229 | 348 |

| 1979 | 2,161 | 960 | 1,201 | 128 | 161 | 40 | 78 | 48 | 67 | 102 | 226 | 352 |

| 1980 | 2,161 | 960 | 1,201 | 129 | 163 | 40 | 77 | 48 | 66 | 102 | 228 | 346 |

| 1981 | 2,143 | 984 | 1,159 | 129 | 162 | 38 | 76 | 47 | 54 | 100 | 232 | 321 |

| 1982 | 2,110 | 990 | 1,121 | 121 | 153 | 38 | 79 | 48 | 57 | 98 | 236 | 291 |

| 1983 | 2,157 | 1,026 | 1,131 | 124 | 152 | 39 | 80 | 50 | 57 | 104 | 239 | 286 |

| 1984 | 2,171 | 1,044 | 1,127 | 119 | 150 | 39 | 79 | 53 | 57 | 109 | 240 | 283 |

| 1985 | 2,252 | 1,107 | 1,145 | 122 | 147 | 40 | 80 | 55 | 56 | 110 | 247 | 286 |

| 1986 | 2,175 | 1,068 | 1,108 | 113 | 138 | 39 | 74 | 56 | 56 | 114 | 240 | 277 |

| 1987 | 2,232 | 1,090 | 1,142 | 117 | 132 | 44 | 74 | 60 | 57 | 125 | 250 | 284 |

| 1988 | 2,222 | 1,050 | 1,172 | 121 | 128 | 48 | 78 | 63 | 58 | 135 | 245 | 297 |

| 1989 | 2,238 | 1,075 | 1,162 | 122 | 127 | 49 | 78 | 66 | 60 | 126 | 246 | 289 |

| 1990 | 2,250 | 1,034 | 1,216 | 123 | 129 | 49 | 78 | 71 | 61 | 132 | 248 | 326 |

| 1991 | 2,243 | 1,013 | 1,230 | 126 | 135 | 50 | 82 | 77 | 64 | 139 | 256 | 302 |

| 1992 | 2,225 | 952 | 1,274 | 128 | 136 | 56 | 85 | 82 | 64 | 133 | 260 | 329 |

| 1993 | 2,157 | 891 | 1,266 | 124 | 135 | 56 | 85 | 82 | 63 | 127 | 268 | 326 |

| 1994 | 2,085 | 850 | 1,235 | 120 | 133 | 55 | 81 | 83 | 59 | 128 | 262 | 315 |

| 1995 | 2,012 | 802 | 1,210 | 113 | 132 | 56 | 76 | 87 | 58 | 128 | 264 | 297 |

| 1996 | 1,934 | 768 | 1,166 | 110 | 130 | 62 | 71 | 88 | 58 | 118 | 251 | 279 |

| 1997 | 1,872 | 723 | 1,149 | 107 | 131 | 64 | 71 | 93 | 59 | 112 | 243 | 270 |

| 1998 | 1,856 | 693 | 1,163 | 106 | 130 | 68 | 72 | 95 | 59 | 112 | 240 | 281 |

| 1999 | 1,820 | 666 | 1,155 | 105 | 130 | 69 | 73 | 97 | 58 | 113 | 219 | 290 |

| 2000 | 1,778 | 651 | 1,127 | 104 | 126 | 70 | 74 | 98 | 58 | 113 | 220 | 265 |

| 2001 | 1,792 | 647 | 1,145 | 109 | 129 | 73 | 76 | 99 | 59 | 117 | 226 | 258 |

| 2002 | 1,818 | 645 | 1,173 | 98 | 130 | 76 | 77 | 96 | 96 | 118 | 223 | 258 |

| 2003 | 1,867 | 636 | 1,231 | 100 | 131 | 153 | 72 | 102 | 58 | 132 | 226 | 257 |

| 2004 | 1,882 | 644 | 1,238 | 111 | 130 | 153 | 77 | 104 | 57 | 111 | 236 | 257 |

| 2005 | 1,872 | 649 | 1,224 | 108 | 131 | 147 | 76 | 105 | 56 | 108 | 235 | 258 |

| 2006 | 1,880 | 653 | 1,227 | 105 | 129 | 154 | 72 | 107 | 54 | 107 | 239 | 260 |

| 2007 | 1,888 | 651 | 1,237 | 103 | 129 | 159 | 72 | 107 | 54 | 104 | 254 | 254 |

| 2008 | 1,960 | 670 | 1,289 | 104 | 132 | 172 | 76 | 109 | 55 | 106 | 274 | 261 |

| 2009 | 2,094 | 737 | 1,357 | 104 | 139 | 180 | 75 | 113 | 57 | 109 | 297 | 283 |

http://www.opm.gov/feddata/HistoricalTables/ExecutiveBranchSince1940.asp

Related Posts On Pronk Palisades

Heritage Foundation 2010 Budget Charts–Federal Spending

Heritage Foundation 2010 Budget Charts–Federal Revenue

Heritage Foundation 2010 Budget Charts–Federal Debt and Deficits

Read Full Post | Make a Comment ( None so far )News Journal: Number 28, October 16, 2010: The Obama Depression Deepens–Federal Reserve Executes–QE II Plan–“Operation Pawnshop”–$2,500 Billion In Quantitative Easing–Money Printing–Will It Be Enough?

Non-conventional vs. Traditional Federal Reserve System Building

“Credit expansion is the governments foremost tool in their struggle against the market economy. In their hands it is the magic wand designed to conjure away the scarcity of capital goods, to lower the rate of interest or to abolish it altogether, to finance lavish government spending, to expropriate the capitalists, to contrive everlasting booms, and to make everybody prosperous.”

“The final outcome of the credit expansion is general impoverishment.”

~Ludwig von Mises

Peter Schiff – It’s Scary How Clueless Bernanke Is

The Gold Dollar | Llewellyn H. Rockwell, Jr.

Fed’s Next Move: What Will Boost the Economy?

Helicopter Ben Bernanke 10/15/10 Part 1

Helicopter Ben Bernanke 10/15/10 Part 2

Swonk Says Bernanke Laid Out Rationale for Fed QE: Video

Currencies, Phillips curve, inflation target, Ramsey, SchiffRadio.com

Bernanke Says Fed Stimulus Move Coming, Amount Unknown

Tyson Says Quantitative Easing ‘Only Policy Option Left’

Jim Grant on Bloomberg 10/8/10: Quantitative Easing Is Just Money Printing

Mandelbrot (Chaos Theory) Taleb (Black Swan) on markets

End the Fed | Ron Paul

The primary goal of the Federal Reserve System is price stability or the avoidance of inflation for the U.S. economy.

However, unlike other central banks, the Federal Reserve also was given several other goals by Congress:

“The goals of monetary policy are spelled out in the Federal Reserve Act, which specifies that the Board of Governors and the Federal Open Market Committee should seek “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” …”

Since the Fed already has a zero interest rate policy or ZIRP with the Federal Funds rate target range of between 0.0% – .25% and a low inflation rate for the time being under 2%, the Federal Reserve now turns it monetary policy tools on the persistent high unemployment rates, now at 9.6% and headed once again to 10% or more.

| Year | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Annual |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2000 | 4.0 | 4.1 | 4.0 | 3.8 | 4.0 | 4.0 | 4.0 | 4.1 | 3.9 | 3.9 | 3.9 | 3.9 | |

| 2001 | 4.2 | 4.2 | 4.3 | 4.4 | 4.3 | 4.5 | 4.6 | 4.9 | 5.0 | 5.3 | 5.5 | 5.7 | |

| 2002 | 5.7 | 5.7 | 5.7 | 5.9 | 5.8 | 5.8 | 5.8 | 5.7 | 5.7 | 5.7 | 5.9 | 6.0 | |

| 2003 | 5.8 | 5.9 | 5.9 | 6.0 | 6.1 | 6.3 | 6.2 | 6.1 | 6.1 | 6.0 | 5.8 | 5.7 | |

| 2004 | 5.7 | 5.6 | 5.8 | 5.6 | 5.6 | 5.6 | 5.5 | 5.4 | 5.4 | 5.5 | 5.4 | 5.4 | |

| 2005 | 5.3 | 5.4 | 5.2 | 5.2 | 5.1 | 5.0 | 5.0 | 4.9 | 5.0 | 5.0 | 5.0 | 4.9 | |

| 2006 | 4.7 | 4.8 | 4.7 | 4.7 | 4.6 | 4.6 | 4.7 | 4.7 | 4.5 | 4.4 | 4.5 | 4.4 | |

| 2007 | 4.6 | 4.5 | 4.4 | 4.5 | 4.4 | 4.6 | 4.6 | 4.6 | 4.7 | 4.7 | 4.7 | 5.0 | |

| 2008 | 5.0 | 4.8 | 5.1 | 5.0 | 5.4 | 5.5 | 5.8 | 6.1 | 6.2 | 6.6 | 6.9 | 7.4 | |

| 2009 | 7.7 | 8.2 | 8.6 | 8.9 | 9.4 | 9.5 | 9.4 | 9.7 | 9.8 | 10.1 | 10.0 | 10.0 | |

| 2010 | 9.7 | 9.7 | 9.7 | 9.9 | 9.7 | 9.5 | 9.5 | 9.6 | 9.6 |

http://data.bls.gov/PDQ/servlet/SurveyOutputServlet

The Chairman of the Federal Reserve, Ben Bernanke, communicated in an October 15, 2010 speech in Boston what the Federal Open Market Committee (FOMC) unconventional monetary policy was targeting– maximum employment–by printing more money and purchasing Treasuries and other bonds:

“…In short, there are clearly many challenges in communicating and conducting monetary policy in a low-inflation environment, including the uncertainties associated with the use of nonconventional policy tools. Despite these challenges, the Federal Reserve remains committed to pursuing policies that promote our dual objectives of maximum employment and price stability. In particular, the FOMC is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation over time to levels consistent with our mandate. …”

Translation, the Fed will be printing more money starting in November to expand the money and credit supply by purchasing Treasury securities including bills, notes and bonds in the market as well other assets such as bonds with the objective of lowering the unemployment rate.

http://nowandfutures.com/key_stats.html

The Fed will be attempting to “inflate” the economy out of the current “jobless recovery” into another economic boom.

Call it quantitative easing, credit easing or “nonconventional” monetary policy, I call it overdosing on interventionism.

Quantitative Easing–Videos

What is the size, scope and duration of the “quantitative easing” or overdosing on interventionism ?

How big will the Fed’s weekly habit be?

My guess it will start “small” with $2 to $5 billion per week and gradually increase to about $15 billion per week?

How long will the Fed persist in this habit before going cold turkey?

At least twelve to forty-eight months or until the unemployment rate is below 6% and core inflation is over 2%.

This will require another massive expansion of the Federal Reserve’s balance sheet.

How much will it take?

My guess is a 1% reduction in the U-3 official unemployment rate would take a minimum of $600 billion per year ($200,000 money or credit expansion times 3,000,000 new jobs in one year)

A 4% reduction in the unemployment rate from 10% to 5% or the creation of about 12,000,000 new jobs would require a minimum of $2,500 billion dollars over four years.

The U.S. official unemployment rate as measured by U-3 is again headed towards 10% with over 15,000,000 Americans unemployed.

The private sector needs to create between 250,000 and 300,000 jobs per month to reduce the official unemployment rate by just .1%.

Currently the private sector is creating less than 100,000 jobs per month.

The United States needs between 100,000 to 150,000 jobs to absorb new entrants into the labor market due to the population growth. There are currently over 1.1 million unemployed new entrants that have not found their first job.

Another 150,000 to 200,000 jobs is are needed to reduce the unemployment by .1%.

Unfortunately, the persistent unemployment problem is even worse.

The U-6 total unemployment rate increased from 16.7% in August to 17.1% in October 2010.

With a total civilian labor force of about 155 million, a 17.1% unemployment rate means that over 26,500,000 Americans are looking for full-time jobs.

This represents over twice the number of unemployed Americans, about 13 million, during the worse month of the Great Depression, March 1933.

Assume it takes a minimum of $200,000 increase in the money and credit supply to create one new job.

Assume it takes 250,000 new jobs per month to reduce the unemployment rate by .1% or 3,000,000 jobs per year to reduce the unemployment rate by 1.2%.

Then the Federal Reserve would need to expand the money and credit supply by about $600 billion per year.

If the objective is to reduce the unemployment rate official unemployment rate U-3 from about 10% to 5% then the Federal Reserve would need to expand the money and credit supply by about $2,500 billion over a forty-eight month period.

I fully expect both the U-3 and U-6 unemployment rates to rise by at least .1 to .2% per month for next three to six months.

This would bring the official unemployment rate or U-3 over 10% during the first quarter of 2011 and the total unemployment rate or U-6 over 18% by the start of the second quarter of 2011.

This would represent over 15 million Americans unemployed and over 28 million seeking full-time unemployment.

This in turn will mean the U.S. economy is entering a “new” recession or a “double dip recession” with declining and most likely negative growth rates in the second and third quarter of 2011 and an increased probability of deflation or a declining general price level for goods and services.

Therefore the case for an expansionary monetary policy is still strong and increasing.

With the Federal Funds rate essentially zero, the Federal Reserve will be purchasing assets such as Treasury securities and agency mortgage-backed securities starting in November and continuing for a least six months until the U.S. unemployment rates are down by at least 1% to 2% or more and growth in production or the gross national product is at least above 3% to 4%.

Assuming the Federal Reserve purchases $12 billion in assets or securities each week, the total amount of the quantitative easing will be about $2,500 billion over the next forty-eight months to bring the official unemployment rate U-3 to about 5%.

The Federal Reserve cannot count upon the central bank of Communist China, the People’s Bank of China, to appreciate the Yuan by more than 5% to 10% per year relative to the U.S. dollar to encourage U.S. exports and reduce Chinese imports to the United States.

The real problem is Federal government spending that should be drastically cut until a balanced or even surplus budget is the result.

The Bush tax rate cuts in 2001 and 2003 need to be made permanent as well.

Until such fiscal economic policies are actually implemented, the only monetary policy “bullets” that the Federal Reserve has left is quantitative easing or money printing to purchase assets by expanding their balance sheet.

The Federal Government has for the last two years run deficits exceeding 1,000 billion each year and totaling over $2,500 billion not counting interest and this is likely to continue for at least one or two years until the U.S. economy fully recovers and the unemployment rates are well below 7%.

These budgetary deficits need to be financed by the Treasury Department issuing Treasury bills, notes and bonds.

The Federal Reserve will monetize some of these Treasury debts as part of its quantitative easing operations to the extent other buyers of Treasuries cannot be found.

What is the size or quantity of the quantitative easing?

I do not expect this to be announced, but at least $2,500 billion may be needed in the next forty-eight months to avoid another recession, significantly reduce unemployment to under 6%, and increase the growth of the economy above 4%.

Will such a “nonconventional” monetary policy work?

Only if the Congress and the President drastically cut the Federal Budget so it balances, do not increase taxes, and repeal Obama care.

In other words,this “nonconventional” monetary policy strategy of asset purchases or quantitative easing is not very likely to work any time soon.

The problem with government intervention into the economy is it always requires even more government intervention to correct past mistakes.

Both fiscal and monetary policy are generating massive uncertainty and a lack of confidence by consumers and businesses results in the deferral of consumption and investment expenditures and the hiring of new employees.

Bernanke understands this for he wrote in his Ph.D. dissertation at M.I.T.:

“…increase uncertainty provides an incentive to defer investments in order to wait for new information.”

Massive increases in the size and scope of the Federal government has resulted in huge budgetary deficits and proposed tax increase during a “jobless recovery”.

These deficits must be financed and the Federal Reserve will make sure that Treasury debt in the form of bills, notes and bonds will be purchased by printing more money as needed.

The Federal Reserve “nonconventional” monetary policy of printing more money is essentially government intervention into the economy to accommodate the U.S. Government’s Department of the Treasury need in financing massive government deficits

The Federal Open Market Committee will purchase Treasuries, mostly short-term Treasury bills but some notes and bonds in exchange for Federal Reserve Notes or money.

While the Fed’s cover story may be that this is needed to reduce unemployment, the real objective is financing massive Federal government spending and deficits. This is similar to what was done from 1942 to 1951 where Treasury long-term government bond yields were fixed at very low levels to finance World War II.

In fact, the Federal Reserve will be debasing the U.S. dollar by reducing the purchasing power of the dollar.

End the Fed | Ron Paul

This is a hidden tax paid by all the American people.

The cost of exports will rise as the U.S. dollar depreciates relative to other foreign currencies.

The price of petroleum will significantly rise and Americans will be paying over $3 a gallon in 2011 and over $4 a gallon in 2012.

The increases in petroleum and gasoline prices will in turn impact food prices.

The Federal Reserve uses a core personal consumption expenditure (PCE) price index approach in measuring and setting inflation targets, which excludes food and energy. The core personal consumption is a less volatile inflation or price measure than a change in total personal consumption expenditures which includes energy and food.

However, the American people need to eat and use gasoline to power their cars and heating oil to warm their homes.

The American people do not tolerate fools, even educated fools of the ruling class, for very long when they are losing their jobs, homes, health care and retirement plans and their children and grandchildren cannot find jobs or complete their college education.

The Second American Revolution has started.

On Tuesday November 2, 2010, election day, a shot will be heard around the world that even the world’s central bankers will be able to hear, if not fully comprehend.

During which the Federal Open Market Committee or FOMC will meet to decide when and how much quantitative easing or credit easing is needed to create jobs, avoid another recession and finance the U.S. government massive deficits.

The U.S. economy is in a liquidity trap where conventional monetary policy is ineffective and “nonconventional” monetary policy cannot work effectively until the appropriate fiscal policies are a reality and working.

The U.S. economy is slowly drowning in a flood of government intervention that has simply failed in generating jobs and high rates of economic growth and wealth creation.

The American people are paying the price for our ruling class’s continuing failures.

After quantitative easing or “operation pawn shop” fails and the value of the U.S. dollars is further debased, a period of inflation will follow and the Obama Depression will become an inflationary depression–a black swan.

“To be told that the Fed did what it could isn’t much comfort to a family who loses its house to foreclosure, a businessman forced into bankruptcy, a sixty-five-year-old whose retirement fund is devastated, a would-be borrower turned away by a beleaguered bank, a new college grad who can’t find a job, any job. For those victims and all the others, a final verdict on the Fed’s response to the Great Panic must await the health of the U.S. economy in 2010 and 2011 and beyond.”

~David Wessle, In Fed We Trust, Ben Bernanke’s War On the Great Panic, page 266.

“It is indeed one of the principal drawbacks of every kind of interventionism that it is so difficult to reverse the process.”

“Economics does not say that isolated government interference with the prices of only one commodity or a few commodities is unfair, bad, or unfeasible. It says that such interference produces results contrary to its purpose, that it makes conditions worse, not better, from the point of view of the government and those backing its interference.”

~Ludwig von Mises

Roubini: U.S. Running Out of Options to Stimulate Economy

Roubini On Double Dip

Nassim Nicholas Taleb – What is a “Black Swan?”

Background Articles and Videos

Peter Schiff “We Should Save ‘Person Of The Year’ For People Who Do Good!

Ron Paul: Allow The Free Market, Not The Fed, To Set Interest Rates

Maynard Keynes Inventor of Quantitative Easing

The Financial Crisis and the Death of Macroeconomics | Joseph T. Salerno

Government’s Response to the Crisis: A Fantastic Success, for Government | Robert Higgs

Why You’ve Never Heard of the Great Depression of 1920 | Thomas E. Woods, Jr.

Keynesian Predictions vs. American History | Thomas E. Woods, Jr.

Our Wise Overlords Are Just Here to Serve Us | Thomas E. Woods. Jr.

Nassim Nicholas Taleb Angry

16. The Evolution and Perfection of Monetary Policy

Crisis and Capitalism

Understanding the Financial Crisis

The Psychology of the Financial Crisis

Money, Banking and the Federal Reserve

How to Abolish the Federal Reserve

Speech

Chairman Ben S. Bernanke

At the Revisiting Monetary Policy in a Low-Inflation Environment Conference, Federal Reserve Bank of Boston, Boston, Massachusetts

October 15, 2010

Monetary Policy Objectives and Tools in a Low-Inflation Environment”…

“…However, possible costs must be weighed against the potential benefits of nonconventional policies. One disadvantage of asset purchases relative to conventional monetary policy is that we have much less experience in judging the economic effects of this policy instrument, which makes it challenging to determine the appropriate quantity and pace of purchases and to communicate this policy response to the public. These factors have dictated that the FOMC proceed with some caution in deciding whether to engage in further purchases of longer-term securities.

Another concern associated with additional securities purchases is that substantial further expansion of the balance sheet could reduce public confidence in the Fed’s ability to execute a smooth exit from its accommodative policies at the appropriate time. Even if unjustified, such a reduction in confidence might lead to an undesired increase in inflation expectations, to a level above the Committee’s inflation objective. To address such concerns and to ensure that it can withdraw monetary accommodation smoothly at the appropriate time, the Federal Reserve has developed an array of new tools.7 With these tools in hand, I am confident that the FOMC will be able to tighten monetary conditions when warranted, even if the balance sheet remains considerably larger than normal at that time.

Central bank communication provides additional means of increasing the degree of policy accommodation when short-term nominal interest rates are near zero. For example, FOMC postmeeting statements have included forward policy guidance since December 2008, and the most recent statements have reflected the FOMC’s anticipation that exceptionally low levels of the federal funds rate are likely to be warranted “for an extended period,” contingent on economic conditions. A step the Committee could consider, if conditions called for it, would be to modify the language of the statement in some way that indicates that the Committee expects to keep the target for the federal funds rate low for longer than markets expect. Such a change would presumably lower longer-term rates by an amount related to the revision in policy expectations. A potential drawback of using the FOMC’s statement in this way is that, at least without a more comprehensive framework in place, it may be difficult to convey the Committee’s policy intentions with sufficient precision and conditionality. The Committee will continue to actively review its communications strategy with the goal of providing as much clarity as possible about its outlook, policy objectives, and policy strategies.

Conclusion

In short, there are clearly many challenges in communicating and conducting monetary policy in a low-inflation environment, including the uncertainties associated with the use of nonconventional policy tools. Despite these challenges, the Federal Reserve remains committed to pursuing policies that promote our dual objectives of maximum employment and price stability. In particular, the FOMC is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation over time to levels consistent with our mandate. Of course, in considering possible further actions, the FOMC will take account of the potential costs and risks of nonconventional policies, and, as always, the Committee’s actions are contingent on incoming information about the economic outlook and financial conditions. ..”

Bernanke sees case for more Federal Reserve easing

“… Federal Reserve Chairman Ben Bernanke on Friday offered his most explicit signal yet that the U.S. central bank was set to ease monetary policy further, but provided no details on how aggressively it might act.

Bernanke warned a prolonged period of high unemployment could choke off the U.S. recovery and that the low level of inflation presented an uncomfortable risk of deflation, a dangerous downward slide in prices.

“There would appear — all else being equal — to be a case for further action,” Bernanke said at a conference sponsored by the Boston Federal Reserve Bank.

With overnight interest rates already close to zero, many economists expect the Fed to launch a fresh round of bond purchases, perhaps on the order of $500 billion, to push borrowing costs lower at its next policy meeting on November 2-3.

Prices for longer-dated U.S. government debt fell after Bernanke’s remarks as investors bet the Fed would be successful in generating more inflation. Stocks were mixed while the dollar briefly hit an eight-month low against the euro.

Bernanke said the central bank could bolster its economy and inflation-lifting efforts by indicating a willingness to hold interest rates low for longer than currently expected.

The Fed pushed overnight rates to zero in December 2008 and then bought $1.7 trillion in U.S. government and mortgage-linked bonds to offer more support for the economy.

Officials have said further asset buying, or quantitative easing, would be the course they would most likely pursue to spur a stronger recovery.

Bernanke indicated Fed policymakers were still weighing how aggressive they should be, leaving markets to guess as to the details of any operation. …”

http://finance.yahoo.com/news/Bernanke-says-sees-case-for-rb-4235164349.html?x=0&.v=3

Personal consumption expenditures price index

“…he PCE price index (PCEPI) (or PCE deflator, PCE price deflator, Implicit Price Deflator for Personal Consumption Expenditures (IPD for PCE) (by the BEA), Chain-type Price Index for Personal Consumption Expenditures (CTPIPCE) (by the FOMC )) is a United States-wide indicator of the average increase in prices for all domestic personal consumption. It is indexed to a base of 100 in 2005. Using a variety of data including U.S. Consumer Price Index and Producer Price Index prices, it is derived from the largest component of the Gross Domestic Product in the BEA’s National Income and Product Accounts, personal consumption expenditures.

The less volatile measure of the PCE price index is the core PCE price index which excludes the more volatile and seasonal food and energy prices.

In comparison to the headline United States Consumer Price Index, which uses one set of expenditure weights for several years, this index uses a Fisher Price Index, which uses expenditure data from both the current period and the preceding period. Also, the PCEPI uses a chained index which compares one quarter’s price to the last quarter’s instead of choosing a fixed base. This price index method assumes that the consumer has made allowances for changes in relative prices. That is to say, they have substituted from goods whose prices are rising to goods whose prices are stable or falling.

The PCE rises about one-third percent less than the CPI, a trend that dates back to 1992. This may be due to the failure of CPI to take into account substitution. Alternatively, an unpublished report on this difference by the BLS suggests that most of it is from different ways of calculating hospital expenses and airfares.[1] …”

http://en.wikipedia.org/wiki/Personal_consumption_expenditures_price_index

Black Swan Theory

“…The Black Swan Theory or “Theory of Black Swan Events” was developed by Nassim Nicholas Taleb to explain: 1) the disproportionate role of high-impact, hard to predict, and rare events that are beyond the realm of normal expectations in history, science, finance and technology, 2) the non-computability of the probability of the consequential rare events using scientific methods (owing to their very nature of small probabilities) and 3) the psychological biases that make people individually and collectively blind to uncertainty and unaware of the massive role of the rare event in historical affairs. Unlike the earlier philosophical “black swan problem”, the “Black Swan Theory” (capitalized) refers only to unexpected events of large magnitude and consequence and their dominant role in history. Such events, considered extreme outliers, collectively play vastly larger roles than regular occurrences.

Black Swan Events were characterized by Nassim Nicholas Taleb in his 2007 book (revised and completed in 2010), The Black Swan. Taleb regards almost all major scientific discoveries, historical events, and artistic accomplishments as “black swans” — undirected and unpredicted. He gives the rise of the Internet, the personal computer, World War I, and the September 11 attacks as examples of Black Swan Events.

The term black swan was a Latin expression — its oldest known reference comes from the poet Juvenal’s characterization of something being “rara avis in terris nigroque simillima cygno” (6.165).[1] In English, this Latin phrase means “a rare bird in the lands, and very like a black swan.” When the phrase was coined, the black swan was presumed not to exist. The importance of the simile lies in its analogy to the fragility of any system of thought. A set of conclusions is potentially undone once any of its fundamental postulates is disproven. In this case, the observation of a single black swan would be the undoing of the phrase’s underlying logic, as well as any reasoning that followed from that underlying logic.

Juvenal’s phrase was a common expression in 16th century London as a statement of impossibility. The London expression derives from the Old World presumption that all swans must be white because all historical records of swans reported that they had white feathers.[2] In that context, a black swan was impossible or at least nonexistent. After a Dutch expedition led by explorer Willem de Vlamingh on the Swan River in 1697, discovered black swans in Western Australia[3], the term metamorphosed to connote that a perceived impossibility might later be disproven. Taleb notes that in the 19th century John Stuart Mill used the black swan logical fallacy as a new term to identify falsification.

Specifically, Taleb asserts[4] in the New York Times:

What we call here a Black Swan (and capitalize it) is an event with the following three attributes.

First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility. Second, it carries an extreme impact. Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.

I stop and summarize the triplet: rarity, extreme impact, and retrospective (though not prospective) predictability. A small number of Black Swans explains almost everything in our world, from the success of ideas and religions, to the dynamics of historical events, to elements of our own personal lives.

Coping with black swan events

The main idea in Taleb’s book is not to attempt to predict Black Swan Events, but to build robustness against negative ones that occur and being able to exploit positive ones. Taleb contends that banks and trading firms are very vulnerable to hazardous Black Swan Events and are exposed to losses beyond that predicted by their defective models.

Taleb states that a Black Swan Event depends on the observer—using a simple example, what may be a Black Swan surprise for a turkey is not a Black Swan surprise for its butcher—hence the objective should be to “avoid being the turkey” by identifying areas of vulnerability in order to “turn the Black Swans white”.

Identifying a black swan event

Based on the author’s criteria:

- The event is a surprise (to the observer).

- The event has a major impact.

- After the fact, the event is rationalized by hindsight, as if it had been expected.

Taleb’s ten principles for a black swan robust world

Taleb enumerates ten principles for building systems that are robust to Black Swan Events:[10]

- What is fragile should break early while it is still small. Nothing should ever become Too Big to Fail.

- No socialisation of losses and privatisation of gains.

- People who were driving a school bus blindfolded (and crashed it) should never be given a new bus.

- Do not let someone making an “incentive” bonus manage a nuclear plant – or your financial risks.

- Counter-balance complexity with simplicity.

- Do not give children sticks of dynamite, even if they come with a warning.

- Only Ponzi schemes should depend on confidence. Governments should never need to “restore confidence”.

- Do not give an addict more drugs if he has withdrawal pains.

- Citizens should not depend on financial assets or fallible “expert” advice for their retirement.

- Make an omelette with the broken eggs.

In addition to these ten principles, Taleb also recommends employing both physical and functional redundancy in the design of systems. These two steps can be found in the principles of resilience architecting. (Reference: Jackson, S. Architecting Resilient Systems: John Wiley & Sons. Hoboken, NJ: 2010.)

http://en.wikipedia.org/wiki/Black_swan_theory

Federal Reserve System: Purposes and Functions

http://www.federalreserve.gov/pf/pdf/pf_complete.pdf

Related Posts On Pronk Palisades

Quantitative Easing–Videos

Cracking Communist Chinese Currency–Float The Yuan/RBN or Devalue Your Currency Via U.S. Dollar 10% Per Year For Next Five Years Or Face U.S. Import Ban–No Pressure–Your Choice–Videos

Chinese Communist State Company–China National Offshore Oil Corp.(CNOOC)–Invests In Texas Oil–Videos

Printing More Money (Quantitative Easing) and The Coming Currency War and Decline In The Purchasing Power of The U.S. Dollar–Robbing The American People–Videos

The Monetarization of The Debt and Quantitative Easing: The Federal Reserve is printing $1,000,000,000,000!–Run-Away Inflation Coming Soon!

Read Full Post | Make a Comment ( None so far )News Journal: Number 26, October 15, 2010: Printing More Money (Quantitative Easing) and The Coming Currency War and Decline In The Purchasing Power of The U.S. Dollar–Robbing The American People–Videos

“True, governments can reduce the rate of interest in the short run. They can issue additional paper money. They can open the way to credit expansion by the banks. They can thus create an artificial boom and the appearance of prosperity. But such a boom is bound to collapse soon or late and to bring about a depression.”

“The gold standard alone makes the determination of moneys purchasing power independent of the ambitions and machinations of governments, of dictators, of political parties, and of pressure groups.”

~Ludwig von Mises

Jim Rogers Currency Wars

“IMF Meeting Stokes Fear of Currency War”

Grant Says Quantitative Easing Is Just Money Printing: Video

Global Currency War Brewing

Is The World On The Verge Of A Currency War?

Daniel Rosen: Currency War

IMF Meeting Stokes Fear of Currency War

Webster Tarpley: “There’s a currency war!”

Heller Says `Very Difficult’ for Fed to Boost Growth: Video

Feldstein Predicts Dollar to Weaken, Boosting Exports: Video

Japan cooperates with US on international currency issues – NHK 101010

US House committee approves China currency bill – NHK 100925

US criticizes China, Japan over currency interventions – NHK 100917

Clyde Prestowitz discusses valuation of Chinese currency

Mar 24 10 Hearing on China’s Exchange Rate Policy, C. Fred Bergsten Opening Statement

Mar 24 10 Hearing on China’s Exchange Rate Policy, Clyde Prestowitz Opening Statement

The Truth About The Economy: Total Collapse

Ron Paul in September 14, 2007

The Federal Reserve System is a banking cartel that benefits the large banks at the expense of the American people.

Cartel economists and so-called experts cannot replace the market by attempting to fix the price of money or the dollar.

Abolish the Federal Reserve System.

Abolish fiat paper currency.

Establish a new United States currency backed by gold.

Milton Friedman on Monetary Policy – 1/3

Milton Friedman on Monetary Policy – 2/3

Milton Friedman on Monetary Policy – 3/3

This is necessary to stop the financing of massive Federal Government deficits by the Federal Reserve that is purchasing U. S. Treasury bills and notes with Federal Reserve Notes by printing money or the monetarization of government debt.

Money printing or quantitative easing decreases the purchasing power of the money supply–debasing of the currency– robbing the American people.

Will the Federal Reserve System and fiat paper money be abolished?

Not any time soon.

The result will first be a longer and deeper recession lasting well into 2013.

In 2013 the Federal Reserve System will be 100 years old.

The Federal Reserves System will celebrate by achieving by then the devaluation of the dollar by 99%.

In other words one dollar in 1913 will be worth 1 cent in 2013.

If this is monetary stability, one wonders what inflation really is.

Time to do away the Federal Reserve System for incompetence.

I do not expect the unemployment rate to fall below 8% for U-3 until 2013 at the earliest.

As unemployment slowly declines in 2011 and 2012, there will be at first a gradual increase in the general price level that will accelerate in 2013.

This will be due the inability of the Federal Reserve to reverse quickly enough its very aggressive expansive monetary policy.

In 2011 and 2012 import prices will rise as the Federal Reserve attempts to devalue the dollar compared with other national currencies in an attempt to expand exports by making them cheaper.

The price of a gallon gasoline in the United States will first rise above $3 in 2011 and $4 in 2012 mainly due to the devaluation of the U.S. dollar.

As Communist China gradually lets the value of its currency rise in value relative to the U.S. dollar, exports from China will rise in price. This means higher prices for goods imported into the U.S. from China.

The decline in the value or purchasing power of the dollar in 2011 and 2012 combined with unemployment rates exceeding 8% will mean further losses for the Democratic Party in 2012 including the Presidency.

The American people are rightfully mad as hell at the ruling class and political elites in Washington D.C.

Power of the Market – How to Cure Inflation 1

Power of the Market – How to Cure Inflation 2

Power of the Market – How to Cure Inflation 3

Ron Paul on the Federal Reserve and Government Deficit Spending

The Gold Standard in Theory and Myth by Joseph Salerno

“The gold standard has one tremendous virtue: the quantity of the money supply, under the gold standard, is independent of the policies of governments and political parties. This is its advantage. It is a form of protection against spendthrift governments.”

“Inflationism, however, is not an isolated phenomenon. It is only one piece in the total framework of politico-economic and socio-philosophical ideas of our time. Just as the sound money policy of gold standard advocates went hand in hand with liberalism, free trade, capitalism and peace, so is inflationism part and parcel of imperialism, militarism, protectionism, statism and socialism.”

~Ludwig von Mises

9. Consolidated Statement of Condition of All Federal Reserve Banks

| Assets, liabilities, and capital | Eliminations from consolidation |

Wednesday Oct 6, 2010 |

Change since | |

|---|---|---|---|---|

| Wednesday Sep 29, 2010 |

Wednesday Oct 7, 2009 |

|||

| Assets | ||||

| Gold certificate account | 11,037 | 0 | 0 | |

| Special drawing rights certificate account | 5,200 | 0 | 0 | |

| Coin | 2,114 | + 3 | + 124 | |

| Securities, repurchase agreements, term auction credit, and other loans |

2,101,199 | + 7,113 | + 216,329 | |

| Securities held outright 1 | 2,051,716 | + 7,403 | + 456,429 | |

| U.S. Treasury securities | 819,072 | + 7,403 | + 49,887 | |

| Bills 2 | 18,423 | 0 | 0 | |

| Notes and bonds, nominal 2 | 752,832 | + 7,390 | + 52,364 | |

| Notes and bonds, inflation-indexed 2 | 42,318 | 0 | – 2,270 | |

| Inflation compensation 3 | 5,499 | + 13 | – 207 | |

| Federal agency debt securities 2 | 154,105 | 0 | + 20,294 | |

| Mortgage-backed securities 4 | 1,078,539 | 0 | + 386,248 | |

| Repurchase agreements 5 | 0 | 0 | 0 | |

| Term auction credit | 0 | 0 | – 178,379 | |

| Other loans | 49,483 | – 290 | – 61,721 | |

| Net portfolio holdings of Commercial Paper Funding Facility LLC 6 |

0 | 0 | – 41,059 | |

| Net portfolio holdings of Maiden Lane LLC 7 | 28,510 | + 40 | + 2,206 | |

| Net portfolio holdings of Maiden Lane II LLC 8 | 15,674 | – 201 | + 1,213 | |

| Net portfolio holdings of Maiden Lane III LLC 9 | 22,782 | – 258 | + 2,616 | |

| Net portfolio holdings of TALF LLC 10 | 601 | 0 | + 601 | |

| Preferred interests in AIA Aurora LLC and ALICO Holdings LLC 11 |

26,057 | + 324 | + 26,057 | |

| Items in process of collection | (84) | 463 | + 98 | + 310 |

| Bank premises | 2,222 | – 7 | + 1 | |

| Central bank liquidity swaps 12 | 61 | 0 | – 49,770 | |

| Other assets 13 | 95,313 | + 2,248 | + 11,389 | |

| Total assets | (84) | 2,311,231 | + 9,358 | + 170,016 |

Note: Components may not sum to totals because of rounding. Footnotes appear at the end of the table. 9. Consolidated Statement of Condition of All Federal Reserve Banks (continued)

| Assets, liabilities, and capital | Eliminations from consolidation |

Wednesday Oct 6, 2010 |

Change since | |

|---|---|---|---|---|

| Wednesday Sep 29, 2010 |

Wednesday Oct 7, 2009 |

|||

| Liabilities | ||||

| Federal Reserve notes, net of F.R. Bank holdings | 918,609 | + 4,849 | + 42,489 | |

| Reverse repurchase agreements 14 | 64,440 | – 2,930 | + 1,540 | |

| Deposits | (0) | 1,253,413 | + 6,593 | + 113,645 |

| Term deposits held by depository institutions | 2,119 | 0 | + 2,119 | |

| Other deposits held by depository institutions | 1,000,014 | + 15,875 | + 33,477 | |

| U.S. Treasury, general account | 49,530 | – 8,299 | + 18,525 | |

| U.S. Treasury, supplementary financing account | 199,962 | + 1 | + 70,006 | |

| Foreign official | 1,345 | – 1,066 | – 540 | |

| Other | (0) | 444 | + 84 | – 9,940 |

| Deferred availability cash items | (84) | 2,598 | + 410 | – 182 |

| Other liabilities and accrued dividends 15 | 15,029 | + 91 | + 6,468 | |

| Total liabilities | (84) | 2,254,089 | + 9,014 | + 163,961 |

| Capital accounts | ||||

| Capital paid in | 26,687 | + 1 | + 1,798 | |

| Surplus | 25,881 | + 6 | + 4,500 | |

| Other capital accounts | 4,575 | + 338 | – 242 | |

| Total capital | 57,142 | + 344 | + 6,055 | |

Note: Components may not sum to totals because of rounding.

1. Includes securities lent to dealers under the overnight and term securities lending facilities; refer to table 1A.

2.Face value of the securities.

3. Compensation that adjusts for the effect of inflation on the original face value of inflation-indexed securities.

11. Refer to table 8.

14. Cash value of agreements, which are collateralized by U.S. Treasury securities, federal agency debt securities, and mortgage-backed securities.

15. Includes the liabilities of Maiden Lane LLC, Maiden Lane II LLC, Maiden Lane III LLC, and TALF LLC to entities other than the Federal Reserve Bank of New York, including liabilities that have recourse only to the portfolio holdings of these LLCs. Refer to table 4 through table 7 and the note on consolidation accompanying table 10.

Minutes of the Federal Open Market Committee September 21, 2010″…At the conclusion of the discussion, the Committee voted to authorize and direct the Federal Reserve Bank of New York, until it was instructed otherwise, to execute transactions in the System Account in accordance with the following domestic policy directive:

“The Federal Open Market Committee seeks monetary and financial conditions that will foster price stability and promote sustainable growth in output. To further its long-run objectives, the Committee seeks conditions in reserve markets consistent with federal funds trading in a range from 0 to 1/4 percent. The Committee directs the Desk to maintain the total face value of domestic securities held in the System Open Market Account at approximately $2 trillion by reinvesting principal payments from agency debt and agency mortgage-backed securities in longer-term Treasury securities. The System Open Market Account Manager and the Secretary will keep the Committee informed of ongoing developments regarding the System’s balance sheet that could affect the attainment over time of the Committee’s objectives of maximum employment and price stability.”

The vote encompassed approval of the statement below to be released at 2:15 p.m.:

“Information received since the Federal Open Market Committee met in August indicates that the pace of recovery in output and employment has slowed in recent months. Household spending is increasing gradually, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. Housing starts are at a depressed level. Bank lending has continued to contract, but at a reduced rate in recent months. The Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, although the pace of economic recovery is likely to be modest in the near term.Measures of underlying inflation are currently at levels somewhat below those the Committee judges most consistent, over the longer run, with its mandate to promote maximum employment and price stability. With substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to remain subdued for some time before rising to levels the Committee considers consistent with its mandate.The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels for the federal funds rate for an extended period. The Committee also will maintain its existing policy of reinvesting principal payments from its securities holdings.The Committee will continue to monitor the economic outlook and financial developments and is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation, over time, to levels consistent with its mandate.”

Voting for this action: Ben Bernanke, William C. Dudley, James Bullard, Elizabeth Duke, Sandra Pianalto, Eric Rosengren, Daniel K. Tarullo, and Kevin Warsh.Voting against this action: Thomas M. Hoenig.Mr. Hoenig dissented, emphasizing that the economy was entering the second year of moderate recovery and that, while the zero interest rate policy and “extended period” language were appropriate during the crisis and its immediate aftermath, they were no longer appropriate with the recovery under way. Mr. Hoenig also emphasized that, in his view, the current high levels of unemployment were not caused by high interest rates but by an extended period of exceptionally low rates earlier in the decade that contributed to the housing bubble and subsequent collapse and recession. He believed that holding rates artificially low would invite the development of new imbalances and undermine long-run growth. He would prefer removing the “extended period” language and thereafter moving the federal funds rate upward, consistent with his views at past meetings that it approach 1 percent, before pausing to determine what further policy actions were needed. Also, given current economic and financial conditions, Mr. Hoenig did not believe that continuing to reinvest principal payments from SOMA securities holdings was required to support the Committee’s policy objectives.It was agreed that the next meeting of the Committee would be held on Tuesday-Wednesday, November 2-3, 2010. The meeting adjourned at 1:10 p.m. on September 21, 2010. …”

http://www.federalreserve.gov/monetarypolicy/fomcminutes20100921.htm

Background Articles and Videos

Marc-Faber– FedsPrinting to Create Final Crisis 8-3-2010

Quantitative easing

Marc Faber Sees Fed Introducing `Massive’ Quantitative Easing

Ron Paul: If You Care About The Poor You Have To Look At Monetary Policy

The Gold Standard Before the Civil War | Murray N. Rothbard

Monetary Policy, Deflation, And Quantitative Easing

“…Aren’t the excess bank reserves inflationary?

Potentially yes, but currently no. Even though banks are earning a meager 25 basis points on their reserves, that is not sufficient incentive to keep large quantities of excess reserves uninvested or unloaned. As they were in the mid-1930s, massive excess reserves are the result of banker fear and uncertainty. The banking system has been saved, but it hasn’t been made whole yet. Bankers continue to worry about reserve levels and liquidity levels and capital levels. They are willing to lend, but only very conservatively to credit-worthy borrowers. Also, much of the slowdown in bank lending comes from low demand for loans by highly qualified borrowers.

The idea that the excess reserves held on banks’ balance sheets should be “mopped up” to prevent them being used in inflationary ways later is a very dangerous idea. They are there voluntarily because bankers feel they are needed. To remove them would cause further bank retrenchment, as it did in the 1930s when the Fed decided to “mop up” the excess reserves of that time.

As the economy and confidence improves, banks will begin using their excess reserves more aggressively. At that point, the Fed will have to be very careful not to stifle that desirable activity on the one hand or let it get out of hand and become inflationary on the other hand. Since they have lots of good, two-handed economists, I think they can pull it off. ..”

http://www.dailymarkets.com/economy/2010/07/30/monetary-policy-deflation-and-quantitative-easing/

The Founding of the Federal Reserve | Murray N. Rothbard

If you work to earn money you need to watch this

Quantitative Easing

“…The term quantitative easing (QE) describes a monetary policy used by central banks to increase the supply of money by increasing the excess reserves of the banking system. This policy is usually invoked when the normal methods to control the money supply have failed, i.e the bank interest rate, discount rate and/or interbank interest rate are either at, or close to, zero.

A central bank implements QE by first crediting its own account with money it creates ex nihilo (“out of nothing”).[1] It then purchases financial assets, including government bonds, agency debt, mortgage-backed securities and corporate bonds, from banks and other financial institutions in a process referred to as open market operations. The purchases, by way of account deposits, give banks the excess reserves required for them to create new money, and thus hopefully induce a stimulation of the economy, by the process of deposit multiplication from increased lending in the fractional reserve banking system.

Risks include the policy being more effective than intended, spurring hyperinflation, or the risk of not being effective enough, if banks opt simply to sit on the additional cash in order to increase their capital reserves in a climate of increasing defaults in their present loan portfolio.[1]

“Quantitative” refers to the fact that a specific quantity of money is being created; “easing” refers to reducing the pressure on banks.[2] However, another explanation is that the name comes from the Japanese-language expression for “stimulatory monetary policy”, which uses the term “easing”.[3] Quantitative easing is sometimes colloquially described as “printing money” although in reality the money is simply created by electronically adding a number to an account. Examples of economies where this policy has been used include Japan during the early 2000s, and the United States, the United Kingdom and the Eurozone during the global financial crisis of 2008–the present, since the programme is suitable for economies where the bank interest rate, discount rate and/or interbank interest rate are either at, or close to, zero.

Concept

Ordinarily, the central bank uses its control of interest rates, or sometimes reserve requirements, to indirectly influence the supply of money.[1] In some situations, such as very low inflation or deflation, setting a low interest rate is not enough to maintain the level of money supply desired by the central bank, and so quantitative easing is employed to further boost the amount of money in the financial system.[1] This is often considered a “last resort” to increase the money supply.[4][5] The first step is for the bank to create more money ex nihilo (“out of nothing”) by crediting its own account. It can then use these funds to buy investments like government bonds from financial firms such as banks, insurance companies and pension funds,[1] in a process known as “monetising the debt“.

For example, in introducing its QE programme, the Bank of England bought gilts from financial institutions, along with a smaller amount of relatively high-quality debt issued by private companies.[6] The banks, insurance companies and pension funds can then use the money they have received for lending or even to buy back more bonds from the bank. The central bank can also lend the new money to private banks or buy assets from banks in exchange for currency.[citation needed] These have the effect of depressing interest yields on government bonds and similar investments, making it cheaper for business to raise capital.[7] Another side effect is that investors will switch to other investments, such as shares, boosting their price and thus creating the illusion of increasing wealth in the economy.[6] QE can reduce interbank overnight interest rates, and thereby encourage banks to loan money to higher interest-paying and financially weaker bodies.

More specifically, the lending undertaken by commercial banks is subject to fractional-reserve banking: they are subject to a regulatory reserve requirement, which requires them to keep a percentage of deposits in “reserve”,[citation needed]: these can only be used to settle transactions between them and the central bank.[7] The remainder, called “excess reserves”, can (but does not have to be) be used as a basis for lending. When, under QE, a central bank buys from an institution, the institution’s bank account is credited directly and their bank gains reserves.[6] The increase in deposits from the quantitative easing process causes an excess in reserves and private banks can then, if they wish, create even more new money out of “thin air” by increasing debt (lending) through a process known as deposit multiplication and thus increase the country’s money supply. The reserve requirement limits the amount of new money. For example a 10% reserve requirement means that for every $10,000 created by quantitative easing the total new money created is potentially $100,000. The US Federal Reserve‘s now out-of-print booklet Modern Money Mechanics explains the process.

A state must be in control of its own currency and monetary policy if it is to unilaterally employ quantitative easing. Countries in the eurozone (for example) cannot unilaterally use this policy tool, but must rely on the European Central Bank to implement it.[citation needed] There may also be other policy considerations. For example, under Article 123 of the Treaty on the Functioning of the European Union[7] and later the Maastricht Treaty, EU member states are not allowed to finance their public deficits (debts) by simply printing the money required to fill the hole, as happened, for example, in Weimar Germany and more recently in Zimbabwe.[1] Banks using QE, such as the Bank of England, have argued that they are increasing the supply of money not to fund government debt but to prevent deflation, and will choose the financial products they buy accordingly, for example, by buying government bonds not straight from the government, but in secondary markets.[1][7]

HistoryQuantitative easing was used unsuccessfully[8] by the Bank of Japan (BOJ) to fight domestic deflation in the early 2000s.[9] During the global financial crisis of 2008–the present, policies announced by the US Federal Reserve under Ben Bernanke to counter the effects of the crisis are a form of quantitative easing. Its balance sheet expanded dramatically by adding new assets and new liabilities without “sterilizing” these by corresponding subtractions. In the same period the United Kingdom used quantitative easing as an additional arm of its monetary policy in order to alleviate its financial crisis.[10][11][12]

The European Central Bank (ECB) has used 12-month long-term refinancing operations (a form of quantitative easing without referring to it as such) through a process of expanding the assets that banks can use as collateral that can be posted to the ECB in return for Euros. This process has led to bonds being “structured for the ECB”[13]. By comparison the other central banks were very restrictive in terms of the collateral they accept: the US Federal Reserve used to accept primarily treasuries (in the first half of 2009 it bought almost any relatively safe dollar-denominated securities); the Bank of England applied a large haircut.

In Japan’s case, the BOJ had been maintaining short-term interest rates at close to their minimum attainable zero values since 1999. With quantitative easing, it flooded commercial banks with excess liquidity to promote private lending, leaving them with large stocks of excess reserves, and therefore little risk of a liquidity shortage.[14] The BOJ accomplished this by buying more government bonds than would be required to set the interest rate to zero. It also bought asset-backed securities and equities, and extended the terms of its commercial paper purchasing operation.[15]

RisksQuantitative easing is seen as a risky strategy that could trigger higher inflation than desired or even hyperinflation if it is improperly used and too much money is created.

Quantitative easing runs the risk of going too far. An increase in money supply to a system has an inflationary effect by diluting the value of a unit of currency. People who have saved money will find it is devalued by inflation; this combined with the associated low interest rates will put people who rely on their savings in difficulty. If devaluation of a currency is seen externally to the country it can affect the international credit rating of the country which in turn can lower the likelihood of foreign investment. Like old-fashioned money printing, Zimbabwe suffered an extreme case of a process that has the same risks as quantitative easing, printing money, making its currency virtually worthless.[1]

…”

http://en.wikipedia.org/wiki/Quantitative_easing

Federal Open Market Committee

“…About the FOMCThe term “monetary policy” refers to the actions undertaken by a central bank, such as the Federal Reserve, to influence the availability and cost of money and credit to help promote national economic goals. The Federal Reserve Act of 1913 gave the Federal Reserve responsibility for setting monetary policy.The Federal Reserve controls the three tools of monetary policy–open market operations, the discount rate, and reserve requirements. The Board of Governors of the Federal Reserve System is responsible for the discount rate and reserve requirements, and the Federal Open Market Committee is responsible for open market operations. Using the three tools, the Federal Reserve influences the demand for, and supply of, balances that depository institutions hold at Federal Reserve Banks and in this way alters the federal funds rate. The federal funds rate is the interest rate at which depository institutions lend balances at the Federal Reserve to other depository institutions overnight.Changes in the federal funds rate trigger a chain of events that affect other short-term interest rates, foreign exchange rates, long-term interest rates, the amount of money and credit, and, ultimately, a range of economic variables, including employment, output, and prices of goods and services.

Structure of the FOMC

The Federal Open Market Committee (FOMC) consists of twelve members–the seven members of the Board of Governors of the Federal Reserve System; the president of the Federal Reserve Bank of New York; and four of the remaining eleven Reserve Bank presidents, who serve one-year terms on a rotating basis. The rotating seats are filled from the following four groups of Banks, one Bank president from each group: Boston, Philadelphia, and Richmond; Cleveland and Chicago; Atlanta, St. Louis, and Dallas; and Minneapolis, Kansas City, and San Francisco. Nonvoting Reserve Bank presidents attend the meetings of the Committee, participate in the discussions, and contribute to the Committee’s assessment of the economy and policy options.The FOMC holds eight regularly scheduled meetings per year. At these meetings, the Committee reviews economic and financial conditions, determines the appropriate stance of monetary policy, and assesses the risks to its long-run goals of price stability and sustainable economic growth.For more detail on the FOMC and monetary policy, see section 2 of the brochure on the structure of the Federal Reserve System and chapter 2 of Purposes & Functions of the Federal Reserve System.

2010 Members of the FOMC

- Members

- Ben S. Bernanke, Board of Governors, Chairman

- William C. Dudley, New York, Vice Chairman

- James Bullard, St. Louis

- Elizabeth A. Duke, Board of Governors

- Thomas M. Hoenig, Kansas City

- Sandra Pianalto, Cleveland

- Sarah Bloom Raskin, Board of Governors

- Eric S. Rosengren, Boston

- Daniel K. Tarullo, Board of Governors

- Kevin M. Warsh, Board of Governors

- Janet L. Yellen, Board of Governors …”

http://www.federalreserve.gov/monetarypolicy/fomc.htm

FEDERAL RESERVE statistical release

H.4.1

Factors Affecting Reserve Balances of Depository Institutions and

Condition Statement of Federal Reserve Banks

Why Chinese Currency Manipulation Is America’s Fault April 15, 2010

“…Unfortunately, the token appreciation that is probably now in store won’t help very much. For one thing, Beijing has played this game before. China first started diversifying its currency reserves away from the dollar (which weakens currency manipulation) in July 2005, and from then until July 2008 allowed the yuan to rise from 8.28 to the dollar to 6.83, where it has since been held nearly steady. But this appreciation, while showcased by China, was purely nominal; after adjusting for inflation, the change was far smaller: about two percent.

How does China manipulate its currency? Mainly by preventing its exporters from using the dollars they earn as they wish. Instead, they are required to swap them for domestic currency at China’s central bank, which then “sterilizes” them by spending them on U.S. Treasury securities (and increasingly other, higher-yielding, investments) rather than U.S. goods. As a result, the price of dollars is propped up — which means the price of yuan is pushed down — by a demand for dollars which doesn’t involve buying American exports.

The amounts involved are astronomical: as of 2008, China’s accumulated dollar-denominated holdings amounted to $1.7 trillion, an astonishing 40 percent of China’s GDP. The China Currency Coalition estimated in 2005 that the yuan was undervalued by 40 percent; past scholarly estimates have ranged from 10 to 75 percent.

Why is this America’s fault? Because China’s currency is manipulated relative to our own only because we permit it, as there is no law requiring us to sell China our bonds and other assets. We could, in fact, end this manipulation at will. All we would need to do is bar China’s purchases, or just tax them to death.

This would be neither an extreme nor an unprecedented move. It is roughly what the Swiss did in 1972, when economic troubles elsewhere in the world generated an excessive flow of money seeking refuge in Swiss franc-denominated assets. This drove up the value of the franc and threatened to make Swiss manufacturing internationally uncompetitive. To prevent this, the Swiss government imposed a number of measures to dampen foreign investment demand for francs, including a ban on the sale of franc-denominated bonds, securities, and real estate to foreigners. Problem solved. (It did not even damage Switzerland’s standing as an international financial center, a key worry at the time.) …”

“…So the real underlying problem is that America doesn’t generate enough savings on its own to meet its voracious appetite for borrowing. China’s savings rate, thanks to deliberate suppression by the Chinese government of its people’s opportunities to spend what they earn, is an astonishing 50 percent. Ours was negative four percent in the last Federal Reserve report on the subject. We are—Oh, how Mao would have loved this!—decadent. …”

http://seekingalpha.com/article/198825-why-chinese-currency-manipulation-is-americas-fault

News Journal: Number 20, September 24, 2010: Eddie Fisher Dies At 82–Videos

By the time I was thirty-three years old I`d been married to America`s sweetheart and America`s femme fatale and both marriages had ended in scandal; I`d been one of the most popular singers in America and had given up my career for love; I had fathered two children and adopted two children and rarely saw any of them; I was addicted to methamphetamines and I couldn`t sleep at night without a huge dose of Librium. And from all this I had learned one very important lesson: There were no rules for me. I could get away with anything so long as that sound came out of my throat.

Pop Singer Eddie Fisher Dies at Age 82

50s pop singer Eddie Fisher dies at age 82