Archive for October, 2010

News Journal: Number 29, October 26, 2010: American People’s No Confidence Voting Wave Wipes Out Democrats–It’s The Economy Stupid!–Videos

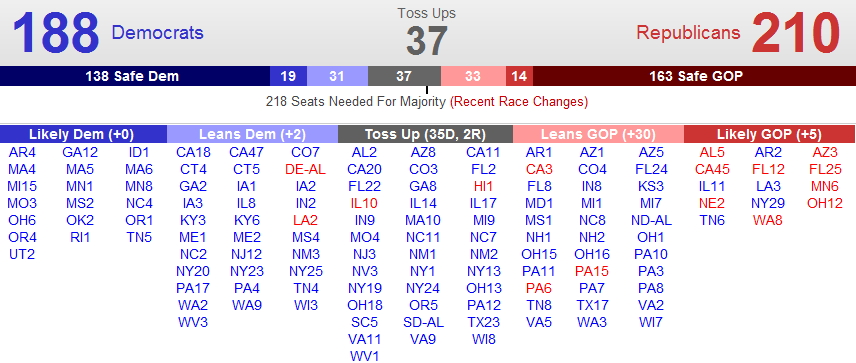

Republican Governors 35

Republican Senators 51

Republican Representatives 255

The Republicans will pickup a net total of 77 seats in House of Representatives for a total of 255.

The Republicans will also pickup a net total of 10 seats in the Senate for a total of 51 seats.

The American people want to stop the massive Government spending, deficits and bailouts and rising National debt of the Obama Administration.

Stop Spending Our Future – The Crisis

Issue number 1 is jobs and the economy with nearly thirty million Americans looking for a full-time job and continuing high rates of unemployment.

Issue number 2 is massive Federal Government spending, deficits, bailouts and a rising National debt.

The National Debt Road Trip

The Trillion $$$ Dollar U.S. Economic Deficit Caused By Our Government

U.S. Debt Clock

Issue number 3 is Obamacare– the American people want it repealed as soon as possible and no money bills or appropriations to fund Obamacare.

Fight Obamacare Texas

Issue number 4 is illegal immigration–the American people want it stopped by immigration law enforcement and a completed border fence that is heavily patrolled.

What Are True Costs And Benefits Of Illegal Immigration?

Stop Illegal Immigration

The American people expect the Republican Party to balance the Federal Budget by significantly reducing Government spending and permanently closing Federal Departments including Agriculture, Commerce, Education, Energy, Health and Human Services, Housing and Urban Development, Interior, Labor, and Transportation.

The number of Federal employees should be cut from over 2,000,000 to less than 1,000,000.

3 Reasons Public Sector Employees are Killing the Economy

The American people expect the Republican Party to make the Bush tax cuts permanent for all taxpayers and pass the FairTax–it is time!

The American people expect the Republican Party to make the Bush tax cuts permanent for all taxpayers and pass the FairTax–it is time!

The FairTax: It’s Time

Should the Republican Party fail to balance the budget and cut the size and scope of the Federal Government by permanently shutting down the above departments, these Republicans will be wiped out by the 2012 wave of tea party patriots.

Background Articles and Videos

Editor in Chief Insights: Obama’s Job Approval Trajectory

President Obama Heads into Midterms at Lowest Approval Rating of Presidency

Two-thirds of Americans believe country going off on the wrong track

“…Currently, two-thirds of Americans (67%) have a negative opinion of the job President Obama is doing while just over one-third (37%) have a positive opinion. This continues the president’s downward trend and he is now at the lowest job approval rating of his presidency.

These are some of the results of The Harris Poll of 3,084 adults surveyed online between October 11 and 18, 2010 by Harris Interactive.

It’s perhaps not surprising that nine in ten Republicans (90%) and Conservatives (89%) give the job the president is doing negative ratings. What may be surprising is that one-third of Democrats (34%) and Liberals (33%) also give him negative ratings, as do seven in ten Independents (70%) and six in ten Moderates (60%).

Americans who give the president the highest positive ratings are those with a post-graduate education (48%), a college education (47%), and those living in the West (42%). On the other end of the spectrum, almost three-quarters of those with a high school education or less (72%) and two-thirds of Midwesterners (66%) and Southerners (66%) give the President negative marks on his overall job.

While the president is at a low point, there is a political body with ratings much lower than his. Just one in ten Americans (11%) give Congress positive ratings on the job they are doing while nine in ten (89%) give them negative marks. While Congress may be under Democratic control, even four in five Democrats (81%) give them negative ratings.

Part of this negativity may have to do with the way Americans believe the country as a whole is going. Just one-third of U.S. adults (34%) say the country is going in the right direction while two-thirds (66%) say it is going off on the wrong track. While not close to the low it was before the 2008 election (11% said things were going in the right direction), this is one of the lower points of this year. …”

http://www.harrisinteractive.com/Hi_assets/TopHitPageNews.html

Rasmussen Reports

Trust on Issues

Voters Trust Republicans More on Eight of 10 Key Issues

“…Voters now trust Democrats over Republicans in only two areas – government ethics and corruption by a 41% to 36% margin and education where Democrats have a slight 42% to 40% edge.

The economy continues to be the most important issue on voters’ minds this election, and 49% place their trust in Republicans to handle this issue. Thirty-nine percent (39%) trust Democrats more. These findings show little change from early June 2009.

On the issue of health care, which voters place second on the list of important issues, Republicans hold a modest 47% to 40% advantage. Democrats were trusted more on this issue until the debate over a proposed national health care bill began to heat up in early September of last year.

Most voters continue to favor repeal of the national health care law, but the number of voters who expect the law to increase the deficit has fallen to the lowest point since its passage by Congress in March.

(Want a free daily e-mail update? If it’s in the news, it’s in our polls). Rasmussen Reports updates are also available on Twitter or Facebook.

Two surveys of 1,000 Likely U.S. Voters each were conducted October 12-13 and October 14-15, 2010 by Rasmussen Reports. The margin of sampling error is +/- 3 percentage points with a 95% level of confidence. Field work for all Rasmussen Reports surveys is conducted by Pulse Opinion Research, LLC. See methodology.

Government ethics and corruption rate number three in terms of overall importance, but voters have been narrowly divided for the past several months over which party to trust more on this issue. Democrats have held small leads since February.

As for education, both parties have held very modest leads on the issue at different times for months now.

Forty-eight percent (48%) of voters nationwide place their trust in the hands of Republicans when it comes to the issue of taxes. Thirty-nine percent (39%) would rather the Democrats handle this issue. The GOP has held a solid lead over Democrats on this issue since early July 2009.

But most voters believe that Democrats in Congress want to raise taxes and spending, while Republicans in Congress want to cut taxes and spending.

When it comes to immigration, 45% trust Republicans, while 33% trust the Democrats more. The gap between the two parties has widened since the beginning of January as the debate over the immigration law in Arizona intensified. At the beginning of the year, voters were essentially evenly divided on which party to trust.

Voters feel more strongly than ever that the federal government is encouraging illegal immigration and that states like Arizona have the answer to the problem, but the Obama administration is challenging the Arizona law in federal court.

Republicans continue to be trusted more on national security issues and the war on terror, with 49% of voters trusting the GOP versus 39% who trust the Democrats more. When it comes the war in Afghanistan, Republicans hold a six-point advantage, 42% to 36%.

Similarly, voters trust Republicans more than Democrats to handle the war in Iraq, 43% to 37%. …”

http://www.rasmussenreports.com/public_content/politics/mood_of_america/trust_on_issues

Historical Federal Workforce Tables

Executive Branch Civilian Employment Since 1940

(end-of-fiscal-year count, excluding Postal Service, in thousands)

| Fiscal Year | Total Executive Branch | Department of Defense | Civilian Agencies | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Total | Agriculture | HHS, Education, Social Sec. 1 | Homeland Security | Interior | Justice | Transportation | Treasury | Veterans | Other | |||

| 1940 | 699 | 256 | 443 | 98 | 9 | 18 | 46 | 11 | … | 45 | 40 | 176 |

| 1941 | 1,081 | 556 | 525 | 91 | 10 | 20 | 50 | 15 | … | 52 | 43 | 244 |

| 1942 | 1,934 | 1,291 | 643 | 95 | 11 | 20 | 49 | 22 | … | 55 | 44 | 348 |

| 1943 | 2,935 | 2,200 | 735 | 109 | 11 | 21 | 43 | 23 | … | 69 | 53 | 406 |

| 1944 | 2,930 | 2,246 | 683 | 78 | 11 | 21 | 42 | 21 | … | 81 | 51 | 378 |

| 1945 | 3,370 | 2,635 | 736 | 82 | 11 | 20 | 45 | 19 | … | 84 | 65 | 409 |

| 1946 | 2,212 | 1,416 | 795 | 97 | 12 | 20 | 51 | 17 | … | 95 | 169 | 335 |

| 1947 | 1,637 | 859 | 777 | 88 | 12 | 20 | 53 | 17 | … | 82 | 217 | 288 |

| 1948 | 1,569 | 871 | 698 | 82 | 13 | 18 | 57 | 20 | … | 79 | 196 | 233 |

| 1949 | 1,573 | 880 | 694 | 87 | 12 | 19 | 59 | 19 | … | 77 | 195 | 226 |

| 1950 | 1,439 | 753 | 686 | 84 | 13 | 20 | 66 | 20 | … | 76 | 188 | 219 |

| 1951 | 1,974 | 1,235 | 738 | 81 | 16 | 21 | 65 | 25 | … | 79 | 183 | 269 |

| 1952 | 2,066 | 1,337 | 729 | 79 | 15 | 22 | 61 | 25 | … | 75 | 175 | 278 |

| 1953 | 2,026 | 1,332 | 694 | 78 | 35 | 22 | 59 | 23 | … | 71 | 178 | 226 |

| 1954 | 1,875 | 1,209 | 666 | 76 | 35 | 21 | 56 | 24 | … | 67 | 179 | 207 |

| 1955 | 1,860 | 1,187 | 673 | 86 | 40 | 21 | 54 | 24 | … | 65 | 178 | 206 |

| 1956 | 1,864 | 1,180 | 684 | 89 | 46 | 20 | 53 | 24 | … | 64 | 177 | 210 |

| 1957 | 1,869 | 1,161 | 708 | 96 | 53 | 20 | 55 | 24 | … | 65 | 174 | 222 |

| 1958 | 1,817 | 1,097 | 720 | 101 | 55 | 20 | 56 | 24 | … | 64 | 172 | 227 |

| 1959 | 1,805 | 1,078 | 727 | 97 | 59 | 20 | 55 | 23 | … | 63 | 171 | 238 |

| 1960 | 1,808 | 1,047 | 761 | 99 | 62 | 21 | 56 | 24 | … | 62 | 172 | 265 |

| 1961 | 1,825 | 1,042 | 782 | 103 | 70 | 20 | 59 | 25 | … | 67 | 175 | 265 |

| 1962 | 1,896 | 1,070 | 827 | 111 | 77 | 20 | 63 | 25 | … | 69 | 177 | 284 |

| 1963 | 1,911 | 1,050 | 861 | 116 | 81 | 21 | 73 | 25 | … | 73 | 173 | 300 |

| 1964 | 1,884 | 1,030 | 855 | 108 | 83 | 21 | 70 | 26 | … | 72 | 172 | 302 |

| 1965 | 1,901 | 1,034 | 867 | 113 | 87 | 21 | 71 | 27 | … | 74 | 167 | 307 |

| 1966 | 2,051 | 1,138 | 913 | 119 | 100 | 21 | 75 | 27 | … | 76 | 170 | 324 |

| 1967 | 2,251 | 1,303 | 949 | 122 | 106 | 24 | 77 | 27 | 52 | 79 | 173 | 289 |

| 1968 | 2,289 | 1,317 | 972 | 123 | 117 | 23 | 78 | 29 | 56 | 79 | 176 | 292 |

| 1969 | 2,301 | 1,342 | 960 | 125 | 113 | 21 | 75 | 30 | 58 | 79 | 175 | 283 |

| 1970 | 2,203 | 1,219 | 983 | 118 | 112 | 23 | 75 | 33 | 62 | 84 | 169 | 308 |

| 1971 | 2,144 | 1,154 | 989 | 120 | 115 | 25 | 72 | 38 | 66 | 86 | 180 | 288 |

| 1972 | 2,117 | 1,108 | 1,009 | 118 | 114 | 29 | 72 | 40 | 65 | 90 | 184 | 295 |

| 1973 | 2,083 | 1,053 | 1,030 | 113 | 128 | 29 | 74 | 43 | 66 | 90 | 198 | 289 |

| 1974 | 2,140 | 1,070 | 1,070 | 116 | 142 | 30 | 77 | 46 | 68 | 97 | 202 | 292 |

| 1975 | 2,149 | 1,042 | 1,107 | 121 | 147 | 31 | 80 | 47 | 69 | 101 | 213 | 297 |

| 1976 | 2,157 | 1,010 | 1,147 | 128 | 155 | 32 | 82 | 48 | 71 | 105 | 222 | 303 |

| 1977 | 2,182 | 1,009 | 1,173 | 132 | 159 | 32 | 87 | 48 | 70 | 107 | 224 | 313 |

| 1978 | 2,224 | 1,000 | 1,225 | 138 | 161 | 37 | 84 | 49 | 70 | 110 | 229 | 348 |

| 1979 | 2,161 | 960 | 1,201 | 128 | 161 | 40 | 78 | 48 | 67 | 102 | 226 | 352 |

| 1980 | 2,161 | 960 | 1,201 | 129 | 163 | 40 | 77 | 48 | 66 | 102 | 228 | 346 |

| 1981 | 2,143 | 984 | 1,159 | 129 | 162 | 38 | 76 | 47 | 54 | 100 | 232 | 321 |

| 1982 | 2,110 | 990 | 1,121 | 121 | 153 | 38 | 79 | 48 | 57 | 98 | 236 | 291 |

| 1983 | 2,157 | 1,026 | 1,131 | 124 | 152 | 39 | 80 | 50 | 57 | 104 | 239 | 286 |

| 1984 | 2,171 | 1,044 | 1,127 | 119 | 150 | 39 | 79 | 53 | 57 | 109 | 240 | 283 |

| 1985 | 2,252 | 1,107 | 1,145 | 122 | 147 | 40 | 80 | 55 | 56 | 110 | 247 | 286 |

| 1986 | 2,175 | 1,068 | 1,108 | 113 | 138 | 39 | 74 | 56 | 56 | 114 | 240 | 277 |

| 1987 | 2,232 | 1,090 | 1,142 | 117 | 132 | 44 | 74 | 60 | 57 | 125 | 250 | 284 |

| 1988 | 2,222 | 1,050 | 1,172 | 121 | 128 | 48 | 78 | 63 | 58 | 135 | 245 | 297 |

| 1989 | 2,238 | 1,075 | 1,162 | 122 | 127 | 49 | 78 | 66 | 60 | 126 | 246 | 289 |

| 1990 | 2,250 | 1,034 | 1,216 | 123 | 129 | 49 | 78 | 71 | 61 | 132 | 248 | 326 |

| 1991 | 2,243 | 1,013 | 1,230 | 126 | 135 | 50 | 82 | 77 | 64 | 139 | 256 | 302 |

| 1992 | 2,225 | 952 | 1,274 | 128 | 136 | 56 | 85 | 82 | 64 | 133 | 260 | 329 |

| 1993 | 2,157 | 891 | 1,266 | 124 | 135 | 56 | 85 | 82 | 63 | 127 | 268 | 326 |

| 1994 | 2,085 | 850 | 1,235 | 120 | 133 | 55 | 81 | 83 | 59 | 128 | 262 | 315 |

| 1995 | 2,012 | 802 | 1,210 | 113 | 132 | 56 | 76 | 87 | 58 | 128 | 264 | 297 |

| 1996 | 1,934 | 768 | 1,166 | 110 | 130 | 62 | 71 | 88 | 58 | 118 | 251 | 279 |

| 1997 | 1,872 | 723 | 1,149 | 107 | 131 | 64 | 71 | 93 | 59 | 112 | 243 | 270 |

| 1998 | 1,856 | 693 | 1,163 | 106 | 130 | 68 | 72 | 95 | 59 | 112 | 240 | 281 |

| 1999 | 1,820 | 666 | 1,155 | 105 | 130 | 69 | 73 | 97 | 58 | 113 | 219 | 290 |

| 2000 | 1,778 | 651 | 1,127 | 104 | 126 | 70 | 74 | 98 | 58 | 113 | 220 | 265 |

| 2001 | 1,792 | 647 | 1,145 | 109 | 129 | 73 | 76 | 99 | 59 | 117 | 226 | 258 |

| 2002 | 1,818 | 645 | 1,173 | 98 | 130 | 76 | 77 | 96 | 96 | 118 | 223 | 258 |

| 2003 | 1,867 | 636 | 1,231 | 100 | 131 | 153 | 72 | 102 | 58 | 132 | 226 | 257 |

| 2004 | 1,882 | 644 | 1,238 | 111 | 130 | 153 | 77 | 104 | 57 | 111 | 236 | 257 |

| 2005 | 1,872 | 649 | 1,224 | 108 | 131 | 147 | 76 | 105 | 56 | 108 | 235 | 258 |

| 2006 | 1,880 | 653 | 1,227 | 105 | 129 | 154 | 72 | 107 | 54 | 107 | 239 | 260 |

| 2007 | 1,888 | 651 | 1,237 | 103 | 129 | 159 | 72 | 107 | 54 | 104 | 254 | 254 |

| 2008 | 1,960 | 670 | 1,289 | 104 | 132 | 172 | 76 | 109 | 55 | 106 | 274 | 261 |

| 2009 | 2,094 | 737 | 1,357 | 104 | 139 | 180 | 75 | 113 | 57 | 109 | 297 | 283 |

http://www.opm.gov/feddata/HistoricalTables/ExecutiveBranchSince1940.asp

Related Posts On Pronk Palisades

Heritage Foundation 2010 Budget Charts–Federal Spending

Heritage Foundation 2010 Budget Charts–Federal Revenue

Heritage Foundation 2010 Budget Charts–Federal Debt and Deficits

Read Full Post | Make a Comment ( None so far )News Journal: Number 28, October 16, 2010: The Obama Depression Deepens–Federal Reserve Executes–QE II Plan–“Operation Pawnshop”–$2,500 Billion In Quantitative Easing–Money Printing–Will It Be Enough?

Non-conventional vs. Traditional Federal Reserve System Building

“Credit expansion is the governments foremost tool in their struggle against the market economy. In their hands it is the magic wand designed to conjure away the scarcity of capital goods, to lower the rate of interest or to abolish it altogether, to finance lavish government spending, to expropriate the capitalists, to contrive everlasting booms, and to make everybody prosperous.”

“The final outcome of the credit expansion is general impoverishment.”

~Ludwig von Mises

Peter Schiff – It’s Scary How Clueless Bernanke Is

The Gold Dollar | Llewellyn H. Rockwell, Jr.

Fed’s Next Move: What Will Boost the Economy?

Helicopter Ben Bernanke 10/15/10 Part 1

Helicopter Ben Bernanke 10/15/10 Part 2

Swonk Says Bernanke Laid Out Rationale for Fed QE: Video

Currencies, Phillips curve, inflation target, Ramsey, SchiffRadio.com

Bernanke Says Fed Stimulus Move Coming, Amount Unknown

Tyson Says Quantitative Easing ‘Only Policy Option Left’

Jim Grant on Bloomberg 10/8/10: Quantitative Easing Is Just Money Printing

Mandelbrot (Chaos Theory) Taleb (Black Swan) on markets

End the Fed | Ron Paul

The primary goal of the Federal Reserve System is price stability or the avoidance of inflation for the U.S. economy.

However, unlike other central banks, the Federal Reserve also was given several other goals by Congress:

“The goals of monetary policy are spelled out in the Federal Reserve Act, which specifies that the Board of Governors and the Federal Open Market Committee should seek “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” …”

Since the Fed already has a zero interest rate policy or ZIRP with the Federal Funds rate target range of between 0.0% – .25% and a low inflation rate for the time being under 2%, the Federal Reserve now turns it monetary policy tools on the persistent high unemployment rates, now at 9.6% and headed once again to 10% or more.

| Year | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Annual |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2000 | 4.0 | 4.1 | 4.0 | 3.8 | 4.0 | 4.0 | 4.0 | 4.1 | 3.9 | 3.9 | 3.9 | 3.9 | |

| 2001 | 4.2 | 4.2 | 4.3 | 4.4 | 4.3 | 4.5 | 4.6 | 4.9 | 5.0 | 5.3 | 5.5 | 5.7 | |

| 2002 | 5.7 | 5.7 | 5.7 | 5.9 | 5.8 | 5.8 | 5.8 | 5.7 | 5.7 | 5.7 | 5.9 | 6.0 | |

| 2003 | 5.8 | 5.9 | 5.9 | 6.0 | 6.1 | 6.3 | 6.2 | 6.1 | 6.1 | 6.0 | 5.8 | 5.7 | |

| 2004 | 5.7 | 5.6 | 5.8 | 5.6 | 5.6 | 5.6 | 5.5 | 5.4 | 5.4 | 5.5 | 5.4 | 5.4 | |

| 2005 | 5.3 | 5.4 | 5.2 | 5.2 | 5.1 | 5.0 | 5.0 | 4.9 | 5.0 | 5.0 | 5.0 | 4.9 | |

| 2006 | 4.7 | 4.8 | 4.7 | 4.7 | 4.6 | 4.6 | 4.7 | 4.7 | 4.5 | 4.4 | 4.5 | 4.4 | |

| 2007 | 4.6 | 4.5 | 4.4 | 4.5 | 4.4 | 4.6 | 4.6 | 4.6 | 4.7 | 4.7 | 4.7 | 5.0 | |

| 2008 | 5.0 | 4.8 | 5.1 | 5.0 | 5.4 | 5.5 | 5.8 | 6.1 | 6.2 | 6.6 | 6.9 | 7.4 | |

| 2009 | 7.7 | 8.2 | 8.6 | 8.9 | 9.4 | 9.5 | 9.4 | 9.7 | 9.8 | 10.1 | 10.0 | 10.0 | |

| 2010 | 9.7 | 9.7 | 9.7 | 9.9 | 9.7 | 9.5 | 9.5 | 9.6 | 9.6 |

http://data.bls.gov/PDQ/servlet/SurveyOutputServlet

The Chairman of the Federal Reserve, Ben Bernanke, communicated in an October 15, 2010 speech in Boston what the Federal Open Market Committee (FOMC) unconventional monetary policy was targeting– maximum employment–by printing more money and purchasing Treasuries and other bonds:

“…In short, there are clearly many challenges in communicating and conducting monetary policy in a low-inflation environment, including the uncertainties associated with the use of nonconventional policy tools. Despite these challenges, the Federal Reserve remains committed to pursuing policies that promote our dual objectives of maximum employment and price stability. In particular, the FOMC is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation over time to levels consistent with our mandate. …”

Translation, the Fed will be printing more money starting in November to expand the money and credit supply by purchasing Treasury securities including bills, notes and bonds in the market as well other assets such as bonds with the objective of lowering the unemployment rate.

http://nowandfutures.com/key_stats.html

The Fed will be attempting to “inflate” the economy out of the current “jobless recovery” into another economic boom.

Call it quantitative easing, credit easing or “nonconventional” monetary policy, I call it overdosing on interventionism.

Quantitative Easing–Videos

What is the size, scope and duration of the “quantitative easing” or overdosing on interventionism ?

How big will the Fed’s weekly habit be?

My guess it will start “small” with $2 to $5 billion per week and gradually increase to about $15 billion per week?

How long will the Fed persist in this habit before going cold turkey?

At least twelve to forty-eight months or until the unemployment rate is below 6% and core inflation is over 2%.

This will require another massive expansion of the Federal Reserve’s balance sheet.

How much will it take?

My guess is a 1% reduction in the U-3 official unemployment rate would take a minimum of $600 billion per year ($200,000 money or credit expansion times 3,000,000 new jobs in one year)

A 4% reduction in the unemployment rate from 10% to 5% or the creation of about 12,000,000 new jobs would require a minimum of $2,500 billion dollars over four years.

The U.S. official unemployment rate as measured by U-3 is again headed towards 10% with over 15,000,000 Americans unemployed.

The private sector needs to create between 250,000 and 300,000 jobs per month to reduce the official unemployment rate by just .1%.

Currently the private sector is creating less than 100,000 jobs per month.

The United States needs between 100,000 to 150,000 jobs to absorb new entrants into the labor market due to the population growth. There are currently over 1.1 million unemployed new entrants that have not found their first job.

Another 150,000 to 200,000 jobs is are needed to reduce the unemployment by .1%.

Unfortunately, the persistent unemployment problem is even worse.

The U-6 total unemployment rate increased from 16.7% in August to 17.1% in October 2010.

With a total civilian labor force of about 155 million, a 17.1% unemployment rate means that over 26,500,000 Americans are looking for full-time jobs.

This represents over twice the number of unemployed Americans, about 13 million, during the worse month of the Great Depression, March 1933.

Assume it takes a minimum of $200,000 increase in the money and credit supply to create one new job.

Assume it takes 250,000 new jobs per month to reduce the unemployment rate by .1% or 3,000,000 jobs per year to reduce the unemployment rate by 1.2%.

Then the Federal Reserve would need to expand the money and credit supply by about $600 billion per year.

If the objective is to reduce the unemployment rate official unemployment rate U-3 from about 10% to 5% then the Federal Reserve would need to expand the money and credit supply by about $2,500 billion over a forty-eight month period.

I fully expect both the U-3 and U-6 unemployment rates to rise by at least .1 to .2% per month for next three to six months.

This would bring the official unemployment rate or U-3 over 10% during the first quarter of 2011 and the total unemployment rate or U-6 over 18% by the start of the second quarter of 2011.

This would represent over 15 million Americans unemployed and over 28 million seeking full-time unemployment.

This in turn will mean the U.S. economy is entering a “new” recession or a “double dip recession” with declining and most likely negative growth rates in the second and third quarter of 2011 and an increased probability of deflation or a declining general price level for goods and services.

Therefore the case for an expansionary monetary policy is still strong and increasing.

With the Federal Funds rate essentially zero, the Federal Reserve will be purchasing assets such as Treasury securities and agency mortgage-backed securities starting in November and continuing for a least six months until the U.S. unemployment rates are down by at least 1% to 2% or more and growth in production or the gross national product is at least above 3% to 4%.

Assuming the Federal Reserve purchases $12 billion in assets or securities each week, the total amount of the quantitative easing will be about $2,500 billion over the next forty-eight months to bring the official unemployment rate U-3 to about 5%.

The Federal Reserve cannot count upon the central bank of Communist China, the People’s Bank of China, to appreciate the Yuan by more than 5% to 10% per year relative to the U.S. dollar to encourage U.S. exports and reduce Chinese imports to the United States.

The real problem is Federal government spending that should be drastically cut until a balanced or even surplus budget is the result.

The Bush tax rate cuts in 2001 and 2003 need to be made permanent as well.

Until such fiscal economic policies are actually implemented, the only monetary policy “bullets” that the Federal Reserve has left is quantitative easing or money printing to purchase assets by expanding their balance sheet.

The Federal Government has for the last two years run deficits exceeding 1,000 billion each year and totaling over $2,500 billion not counting interest and this is likely to continue for at least one or two years until the U.S. economy fully recovers and the unemployment rates are well below 7%.

These budgetary deficits need to be financed by the Treasury Department issuing Treasury bills, notes and bonds.

The Federal Reserve will monetize some of these Treasury debts as part of its quantitative easing operations to the extent other buyers of Treasuries cannot be found.

What is the size or quantity of the quantitative easing?

I do not expect this to be announced, but at least $2,500 billion may be needed in the next forty-eight months to avoid another recession, significantly reduce unemployment to under 6%, and increase the growth of the economy above 4%.

Will such a “nonconventional” monetary policy work?

Only if the Congress and the President drastically cut the Federal Budget so it balances, do not increase taxes, and repeal Obama care.

In other words,this “nonconventional” monetary policy strategy of asset purchases or quantitative easing is not very likely to work any time soon.

The problem with government intervention into the economy is it always requires even more government intervention to correct past mistakes.

Both fiscal and monetary policy are generating massive uncertainty and a lack of confidence by consumers and businesses results in the deferral of consumption and investment expenditures and the hiring of new employees.

Bernanke understands this for he wrote in his Ph.D. dissertation at M.I.T.:

“…increase uncertainty provides an incentive to defer investments in order to wait for new information.”

Massive increases in the size and scope of the Federal government has resulted in huge budgetary deficits and proposed tax increase during a “jobless recovery”.

These deficits must be financed and the Federal Reserve will make sure that Treasury debt in the form of bills, notes and bonds will be purchased by printing more money as needed.

The Federal Reserve “nonconventional” monetary policy of printing more money is essentially government intervention into the economy to accommodate the U.S. Government’s Department of the Treasury need in financing massive government deficits

The Federal Open Market Committee will purchase Treasuries, mostly short-term Treasury bills but some notes and bonds in exchange for Federal Reserve Notes or money.

While the Fed’s cover story may be that this is needed to reduce unemployment, the real objective is financing massive Federal government spending and deficits. This is similar to what was done from 1942 to 1951 where Treasury long-term government bond yields were fixed at very low levels to finance World War II.

In fact, the Federal Reserve will be debasing the U.S. dollar by reducing the purchasing power of the dollar.

End the Fed | Ron Paul

This is a hidden tax paid by all the American people.

The cost of exports will rise as the U.S. dollar depreciates relative to other foreign currencies.

The price of petroleum will significantly rise and Americans will be paying over $3 a gallon in 2011 and over $4 a gallon in 2012.

The increases in petroleum and gasoline prices will in turn impact food prices.

The Federal Reserve uses a core personal consumption expenditure (PCE) price index approach in measuring and setting inflation targets, which excludes food and energy. The core personal consumption is a less volatile inflation or price measure than a change in total personal consumption expenditures which includes energy and food.

However, the American people need to eat and use gasoline to power their cars and heating oil to warm their homes.

The American people do not tolerate fools, even educated fools of the ruling class, for very long when they are losing their jobs, homes, health care and retirement plans and their children and grandchildren cannot find jobs or complete their college education.

The Second American Revolution has started.

On Tuesday November 2, 2010, election day, a shot will be heard around the world that even the world’s central bankers will be able to hear, if not fully comprehend.

During which the Federal Open Market Committee or FOMC will meet to decide when and how much quantitative easing or credit easing is needed to create jobs, avoid another recession and finance the U.S. government massive deficits.

The U.S. economy is in a liquidity trap where conventional monetary policy is ineffective and “nonconventional” monetary policy cannot work effectively until the appropriate fiscal policies are a reality and working.

The U.S. economy is slowly drowning in a flood of government intervention that has simply failed in generating jobs and high rates of economic growth and wealth creation.

The American people are paying the price for our ruling class’s continuing failures.

After quantitative easing or “operation pawn shop” fails and the value of the U.S. dollars is further debased, a period of inflation will follow and the Obama Depression will become an inflationary depression–a black swan.

“To be told that the Fed did what it could isn’t much comfort to a family who loses its house to foreclosure, a businessman forced into bankruptcy, a sixty-five-year-old whose retirement fund is devastated, a would-be borrower turned away by a beleaguered bank, a new college grad who can’t find a job, any job. For those victims and all the others, a final verdict on the Fed’s response to the Great Panic must await the health of the U.S. economy in 2010 and 2011 and beyond.”

~David Wessle, In Fed We Trust, Ben Bernanke’s War On the Great Panic, page 266.

“It is indeed one of the principal drawbacks of every kind of interventionism that it is so difficult to reverse the process.”

“Economics does not say that isolated government interference with the prices of only one commodity or a few commodities is unfair, bad, or unfeasible. It says that such interference produces results contrary to its purpose, that it makes conditions worse, not better, from the point of view of the government and those backing its interference.”

~Ludwig von Mises

Roubini: U.S. Running Out of Options to Stimulate Economy

Roubini On Double Dip

Nassim Nicholas Taleb – What is a “Black Swan?”

Background Articles and Videos

Peter Schiff “We Should Save ‘Person Of The Year’ For People Who Do Good!

Ron Paul: Allow The Free Market, Not The Fed, To Set Interest Rates

Maynard Keynes Inventor of Quantitative Easing

The Financial Crisis and the Death of Macroeconomics | Joseph T. Salerno

Government’s Response to the Crisis: A Fantastic Success, for Government | Robert Higgs

Why You’ve Never Heard of the Great Depression of 1920 | Thomas E. Woods, Jr.

Keynesian Predictions vs. American History | Thomas E. Woods, Jr.

Our Wise Overlords Are Just Here to Serve Us | Thomas E. Woods. Jr.

Nassim Nicholas Taleb Angry

16. The Evolution and Perfection of Monetary Policy

Crisis and Capitalism

Understanding the Financial Crisis

The Psychology of the Financial Crisis

Money, Banking and the Federal Reserve

How to Abolish the Federal Reserve

Speech

Chairman Ben S. Bernanke

At the Revisiting Monetary Policy in a Low-Inflation Environment Conference, Federal Reserve Bank of Boston, Boston, Massachusetts

October 15, 2010

Monetary Policy Objectives and Tools in a Low-Inflation Environment”…

“…However, possible costs must be weighed against the potential benefits of nonconventional policies. One disadvantage of asset purchases relative to conventional monetary policy is that we have much less experience in judging the economic effects of this policy instrument, which makes it challenging to determine the appropriate quantity and pace of purchases and to communicate this policy response to the public. These factors have dictated that the FOMC proceed with some caution in deciding whether to engage in further purchases of longer-term securities.

Another concern associated with additional securities purchases is that substantial further expansion of the balance sheet could reduce public confidence in the Fed’s ability to execute a smooth exit from its accommodative policies at the appropriate time. Even if unjustified, such a reduction in confidence might lead to an undesired increase in inflation expectations, to a level above the Committee’s inflation objective. To address such concerns and to ensure that it can withdraw monetary accommodation smoothly at the appropriate time, the Federal Reserve has developed an array of new tools.7 With these tools in hand, I am confident that the FOMC will be able to tighten monetary conditions when warranted, even if the balance sheet remains considerably larger than normal at that time.

Central bank communication provides additional means of increasing the degree of policy accommodation when short-term nominal interest rates are near zero. For example, FOMC postmeeting statements have included forward policy guidance since December 2008, and the most recent statements have reflected the FOMC’s anticipation that exceptionally low levels of the federal funds rate are likely to be warranted “for an extended period,” contingent on economic conditions. A step the Committee could consider, if conditions called for it, would be to modify the language of the statement in some way that indicates that the Committee expects to keep the target for the federal funds rate low for longer than markets expect. Such a change would presumably lower longer-term rates by an amount related to the revision in policy expectations. A potential drawback of using the FOMC’s statement in this way is that, at least without a more comprehensive framework in place, it may be difficult to convey the Committee’s policy intentions with sufficient precision and conditionality. The Committee will continue to actively review its communications strategy with the goal of providing as much clarity as possible about its outlook, policy objectives, and policy strategies.

Conclusion

In short, there are clearly many challenges in communicating and conducting monetary policy in a low-inflation environment, including the uncertainties associated with the use of nonconventional policy tools. Despite these challenges, the Federal Reserve remains committed to pursuing policies that promote our dual objectives of maximum employment and price stability. In particular, the FOMC is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation over time to levels consistent with our mandate. Of course, in considering possible further actions, the FOMC will take account of the potential costs and risks of nonconventional policies, and, as always, the Committee’s actions are contingent on incoming information about the economic outlook and financial conditions. ..”

Bernanke sees case for more Federal Reserve easing

“… Federal Reserve Chairman Ben Bernanke on Friday offered his most explicit signal yet that the U.S. central bank was set to ease monetary policy further, but provided no details on how aggressively it might act.

Bernanke warned a prolonged period of high unemployment could choke off the U.S. recovery and that the low level of inflation presented an uncomfortable risk of deflation, a dangerous downward slide in prices.

“There would appear — all else being equal — to be a case for further action,” Bernanke said at a conference sponsored by the Boston Federal Reserve Bank.

With overnight interest rates already close to zero, many economists expect the Fed to launch a fresh round of bond purchases, perhaps on the order of $500 billion, to push borrowing costs lower at its next policy meeting on November 2-3.

Prices for longer-dated U.S. government debt fell after Bernanke’s remarks as investors bet the Fed would be successful in generating more inflation. Stocks were mixed while the dollar briefly hit an eight-month low against the euro.

Bernanke said the central bank could bolster its economy and inflation-lifting efforts by indicating a willingness to hold interest rates low for longer than currently expected.

The Fed pushed overnight rates to zero in December 2008 and then bought $1.7 trillion in U.S. government and mortgage-linked bonds to offer more support for the economy.

Officials have said further asset buying, or quantitative easing, would be the course they would most likely pursue to spur a stronger recovery.

Bernanke indicated Fed policymakers were still weighing how aggressive they should be, leaving markets to guess as to the details of any operation. …”

http://finance.yahoo.com/news/Bernanke-says-sees-case-for-rb-4235164349.html?x=0&.v=3

Personal consumption expenditures price index

“…he PCE price index (PCEPI) (or PCE deflator, PCE price deflator, Implicit Price Deflator for Personal Consumption Expenditures (IPD for PCE) (by the BEA), Chain-type Price Index for Personal Consumption Expenditures (CTPIPCE) (by the FOMC )) is a United States-wide indicator of the average increase in prices for all domestic personal consumption. It is indexed to a base of 100 in 2005. Using a variety of data including U.S. Consumer Price Index and Producer Price Index prices, it is derived from the largest component of the Gross Domestic Product in the BEA’s National Income and Product Accounts, personal consumption expenditures.

The less volatile measure of the PCE price index is the core PCE price index which excludes the more volatile and seasonal food and energy prices.

In comparison to the headline United States Consumer Price Index, which uses one set of expenditure weights for several years, this index uses a Fisher Price Index, which uses expenditure data from both the current period and the preceding period. Also, the PCEPI uses a chained index which compares one quarter’s price to the last quarter’s instead of choosing a fixed base. This price index method assumes that the consumer has made allowances for changes in relative prices. That is to say, they have substituted from goods whose prices are rising to goods whose prices are stable or falling.

The PCE rises about one-third percent less than the CPI, a trend that dates back to 1992. This may be due to the failure of CPI to take into account substitution. Alternatively, an unpublished report on this difference by the BLS suggests that most of it is from different ways of calculating hospital expenses and airfares.[1] …”

http://en.wikipedia.org/wiki/Personal_consumption_expenditures_price_index

Black Swan Theory

“…The Black Swan Theory or “Theory of Black Swan Events” was developed by Nassim Nicholas Taleb to explain: 1) the disproportionate role of high-impact, hard to predict, and rare events that are beyond the realm of normal expectations in history, science, finance and technology, 2) the non-computability of the probability of the consequential rare events using scientific methods (owing to their very nature of small probabilities) and 3) the psychological biases that make people individually and collectively blind to uncertainty and unaware of the massive role of the rare event in historical affairs. Unlike the earlier philosophical “black swan problem”, the “Black Swan Theory” (capitalized) refers only to unexpected events of large magnitude and consequence and their dominant role in history. Such events, considered extreme outliers, collectively play vastly larger roles than regular occurrences.

Black Swan Events were characterized by Nassim Nicholas Taleb in his 2007 book (revised and completed in 2010), The Black Swan. Taleb regards almost all major scientific discoveries, historical events, and artistic accomplishments as “black swans” — undirected and unpredicted. He gives the rise of the Internet, the personal computer, World War I, and the September 11 attacks as examples of Black Swan Events.

The term black swan was a Latin expression — its oldest known reference comes from the poet Juvenal’s characterization of something being “rara avis in terris nigroque simillima cygno” (6.165).[1] In English, this Latin phrase means “a rare bird in the lands, and very like a black swan.” When the phrase was coined, the black swan was presumed not to exist. The importance of the simile lies in its analogy to the fragility of any system of thought. A set of conclusions is potentially undone once any of its fundamental postulates is disproven. In this case, the observation of a single black swan would be the undoing of the phrase’s underlying logic, as well as any reasoning that followed from that underlying logic.

Juvenal’s phrase was a common expression in 16th century London as a statement of impossibility. The London expression derives from the Old World presumption that all swans must be white because all historical records of swans reported that they had white feathers.[2] In that context, a black swan was impossible or at least nonexistent. After a Dutch expedition led by explorer Willem de Vlamingh on the Swan River in 1697, discovered black swans in Western Australia[3], the term metamorphosed to connote that a perceived impossibility might later be disproven. Taleb notes that in the 19th century John Stuart Mill used the black swan logical fallacy as a new term to identify falsification.

Specifically, Taleb asserts[4] in the New York Times:

What we call here a Black Swan (and capitalize it) is an event with the following three attributes.

First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility. Second, it carries an extreme impact. Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.

I stop and summarize the triplet: rarity, extreme impact, and retrospective (though not prospective) predictability. A small number of Black Swans explains almost everything in our world, from the success of ideas and religions, to the dynamics of historical events, to elements of our own personal lives.

Coping with black swan events

The main idea in Taleb’s book is not to attempt to predict Black Swan Events, but to build robustness against negative ones that occur and being able to exploit positive ones. Taleb contends that banks and trading firms are very vulnerable to hazardous Black Swan Events and are exposed to losses beyond that predicted by their defective models.

Taleb states that a Black Swan Event depends on the observer—using a simple example, what may be a Black Swan surprise for a turkey is not a Black Swan surprise for its butcher—hence the objective should be to “avoid being the turkey” by identifying areas of vulnerability in order to “turn the Black Swans white”.

Identifying a black swan event

Based on the author’s criteria:

- The event is a surprise (to the observer).

- The event has a major impact.

- After the fact, the event is rationalized by hindsight, as if it had been expected.

Taleb’s ten principles for a black swan robust world

Taleb enumerates ten principles for building systems that are robust to Black Swan Events:[10]

- What is fragile should break early while it is still small. Nothing should ever become Too Big to Fail.

- No socialisation of losses and privatisation of gains.

- People who were driving a school bus blindfolded (and crashed it) should never be given a new bus.

- Do not let someone making an “incentive” bonus manage a nuclear plant – or your financial risks.

- Counter-balance complexity with simplicity.

- Do not give children sticks of dynamite, even if they come with a warning.

- Only Ponzi schemes should depend on confidence. Governments should never need to “restore confidence”.

- Do not give an addict more drugs if he has withdrawal pains.

- Citizens should not depend on financial assets or fallible “expert” advice for their retirement.

- Make an omelette with the broken eggs.

In addition to these ten principles, Taleb also recommends employing both physical and functional redundancy in the design of systems. These two steps can be found in the principles of resilience architecting. (Reference: Jackson, S. Architecting Resilient Systems: John Wiley & Sons. Hoboken, NJ: 2010.)

http://en.wikipedia.org/wiki/Black_swan_theory

Federal Reserve System: Purposes and Functions

http://www.federalreserve.gov/pf/pdf/pf_complete.pdf

Related Posts On Pronk Palisades

Quantitative Easing–Videos

Cracking Communist Chinese Currency–Float The Yuan/RBN or Devalue Your Currency Via U.S. Dollar 10% Per Year For Next Five Years Or Face U.S. Import Ban–No Pressure–Your Choice–Videos

Chinese Communist State Company–China National Offshore Oil Corp.(CNOOC)–Invests In Texas Oil–Videos

Printing More Money (Quantitative Easing) and The Coming Currency War and Decline In The Purchasing Power of The U.S. Dollar–Robbing The American People–Videos

The Monetarization of The Debt and Quantitative Easing: The Federal Reserve is printing $1,000,000,000,000!–Run-Away Inflation Coming Soon!

Read Full Post | Make a Comment ( None so far )News Journal: Number 27, October 16, 2010: Cracking Communist Chinese Currency–Float The Yuan/RBN or Devalue Your Currency Via U.S. Dollar 10% Per Year For Next Five Years Or Face U.S. Import Ban–No Pressure–Your Choice–Videos

“The valuation of the monetary unit depends not upon the wealth of the country, but upon the ratio between the quantity of money and the demand for it, so that even the richest country may have a bad currency and the poorest country a good one.”

~Ludwig von Mises, The Theory of Money and Credit, page 278.

“The peculiar character of the problem of a rational economic order is determined precisely by the fact that the knowledge of the circumstances of which we must make use never exists in concentrated or integrated form but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess. The economic problem of society is thus not merely a problem of how to allocate “given” resources—if “given” is taken to mean given to a single mind which deliberately solves the problem set by these “data.” It is rather a problem of how to secure the best use of resources known to any of the members of society, for ends whose relative importance only these individuals know. Or, to put it briefly, it is a problem of the utilization of knowledge which is not given to anyone in its totality.”

~Friedrich A. Hayek, The Use of Knowledge in Society

September, 1945, American Economic Review. XXXV, No. 4. pp. 519-30. American Economic Association

http://www.econlib.org/library/Essays/hykKnw1.html

Capitalism in China: Should We Trade With Them? – Ayn Rand Center for Individual Rights

Dr. Milton Friedman speaking about Free Trade

The looming China-U.S. showdown

Battling over the Yuan – F24 101001

China’s Wen Jiabao: ‘Dont pressure us to raise RMB rates’

Lee Says China Will Appreciate Yuan to Prevent Trade War: Video

Eurozone troika urges ‘broad-based’ currency appreciation in China

Inside Look: China Currency Controversy

China Currency and Trade Wars

Peter Schiff – June 21 2010 – Appreciation Of The Chinese Currency Means The Implosion Of The Dollar

Mar 24 10 Hearing on China’s Exchange Rate Policy, Niall Ferguson Opening Statement

Mar 24 10 Hearing on China’s Exchange Rate Policy, C. Fred Bergsten Opening Statement

Mar 24 10 Hearing on China’s Exchange Rate Policy, Clyde Prestowitz Opening Statement

Mar 24 10 Hearing on China’s Exchange Rate Policy, Philip Levy Opening Statement

The U.S. and China (Ted Galen Carpenter)

Government intervention into markets always requires even more government intervention to correct past mistakes.

The central bank of the People’s Republic of China (PRC) would be well advised to just let their currency freely float against the currencies of the world.

This would mean the PRC’s official currency the renminbi or RMB and its unit of currency the yuan would rise in value against both the U.S. dollar and the Euro.

Yes, this would mean the PRC’s export goods would be more expensive for both Americans and Europeans and conversely American and European goods and services would be cheaper to purchase for the PRC.

The result would be a decline in the growth of exports to the United States and Europe.

The Chinese people need to be able to increase their level of consumption and reduce their savings rate to absorb the production that currently goes almost entirely abroad as exports.

Should the PRC implement such a strategy, it would be advised to stop purchasing United States Treasury debt and as the U.S Treasury obligations mature use the dollar payments to purchase natural resource assets in the United States.

In other words diversify your portfolio out foreign government obligations into natural resources that your economy needs to manufacture goods.

As a second best solution, gradually appreciate the renminbi against the U.S. dollar at 10% per year for five years and then freely float the yuan.

Since the U.S unemployment rate is expected to exceed 8% for at least the next three years, the appreciation of the renminbi at 10% a year for five years would lead to a decline in U.S. unemployment due to increase in U.S. exports and and a rise in the demand for Chinese exports as the U.S economy recovers from the recession.

Absence an improvement in the U.S. employment situation, demand for Chinese exports would be flat or even decline.

Therefore, it is in the interest of both countries governments to have an appreciation of the renminbi.

The U.S. Federal Reserve should also abandon its practice of intervening in the U.S money market by attempting to set target Federal fund rates to expand the money supply and in turn credit.

Will any of the above actually happen?

Not likely.

The ruling classes of United States and the People’s Republic of China actually believe they are have the intelligence and knowledge exceeding that of free markets.

Both ruling classes are only fooling themselves.

Both are wrong.

Let the currency wars begin.

Let the ruling class of both parties demonstrate they care less for the welfare of their people.

Let the American and Chinese people determine the fates of their ruling class.

Increasing unemployment in both countries will lead to a revolution and the overthrow of both ruling classes.

The free market will over time prevail and the ruling class control freaks with their failed government interventionist economic policies will be replaced.

Power of the Market – How to Cure Inflation 1

Power of the Market – How to Cure Inflation 2

Power of the Market – How to Cure Inflation 3

“We shall not grow wiser before we learn that much that we have done was very foolish. “

~Friedrich A. Hayek

“Perpetual vigilance on the part of the citizens can achieve what a thousand laws and dozens of alphabetical bureaus with hordes of employees never have and never will achieve: the preservation of a sound currency.”

~Ludwig von Mises, The Theory of Money and Credit, page 495

Background Articles and Videos

China’s Economy in the Post-Crisis World

Obama Pressed On New Global Currency At Presidential News Conference

Related Posts On Pronk Palisades

Chinese Communist State Company–China National Offshore Oil Corp.(CNOOC)–Invests In Texas Oil–Videos

Printing More Money (Quantitative Easing) and The Coming Currency War and Decline In The Purchasing Power of The U.S. Dollar–Robbing The American People–Videos

The Monetarization of The Debt and Quantitative Easing: The Federal Reserve is printing $1,000,000,000,000!–Run-Away Inflation Coming Soon!

Read Full Post | Make a Comment ( None so far )

Producing Dialogue–Videos

ADR. What is ADR? Automated Dialogue Replacement

Automated Dialogue Replacement

EXTRAORDINARY Webdoc 10: POSTPRODUCTION – ADR Voice Overs

Post Synchronization

1. Influences of nonverbal speech on meaning include accent, pace, patterns, emphasis, inflection and mood.

2. The principal challenge during production is recording dialogue that is clear, intelligible, and as noise-free as possible.

3. Dramatizations on radio involve creating a “theater of the mind,” using sound to impel the listener to “see” the action.

4. To create perspective using one microphone n radio dramatization, performers are positioned at appropriate distances relative to the mic and to one another, as the dramatic action dictates.

5. Using the multimicrophone technique in radio dramatization, perspective is created in the postproduction mix.

6. For stereo radio dramatizations, coincident or near-coincident microphone arrays are usually employed. Coincident miking positions two microphones, usually directional (or s stereo mic), in virtually the same space, with their diaphragms located vertically on the same axis. Near-coincident miking positions two mics, usually directional, horizontally on the same plane, angled a few inches apart.

7. A main difference and advantages of surround-sound miking radio dramatizations is being able to position performers much as they would be on a stage and recording them from those perspectives or recording them conventionally and creating those perspectives in postproduction.

8. Recording dialogue on the set of a multi- or single-camera production usually means employing a boom, body-mounted wireless, or plant microphone, or a combination of the three. The microphones of choice are usually the mini- and shotgun capacitor mics.

9. The main sonic difference between the boom and body-mounted microphones is perspective. The boom better reproduces the mic-to-source distances that are relative to the shots’ fields of view. This helps maintain acoustic perspective between sound and picture. on the other hand, the body-mounted mic always picks up dialogue that is clear and present with a minimum of background sound, but sonic perspective remains the same regardless of a shot’s focal length.

10. Miking decisions are made in preproduction planning during blocking, when the movements of performers and cameras are worked out.

11. The challenge in operating a boom is to maintain aural perspective while simultaneously keeping the performers in the mic’s pickup pattern and, of course, the mic out of the frame.

12. Care must be taken when using a body mic to ensure that it is inconspicuous and that it does not pick up the sound of clothes rustling. Cotton does not make as much rustling sound as do synthetic fabrics.

13. Plant, or fixed, microphones are positioned around a set to cover action that cannot easily be picked up with a boom or body mic.

14. Preproduction planning is essential in any production, but especially so when working in the field, away from security and resources of the studio. Preproduction planning involves selecting a location; determining how to deal with unwanted sound; preparing, in advance, prerecorded material; and anticipating all the main and backup equipment needs.

15. In production, recording the clearest, most intelligible noise-free dialogue is the primary challenge of the production recordist, regardless of a director’s intention to use it or redo it in postproduction.

16. Dealing with unwanted sound on the set is an ever-present challenge to the audio crew. But being aware of problems is not enough–ou have to know what, if anything, to do about them.

17. Be wary of employing signal processing during production recording. It affects the dialogue audio throughout postproduction.

18. The value of noise reduction throughout the production process cannot be overemphasized, especially in relation to dialogue and field recording.

19. If the director enlightens the entire picture-producing team on how to avoid or minimize audio problems, it goes a long way toward audio efficiency and economy, not only in production but in postproduction as well.

20. Production recordists can be of considerable help in giving sound editors flexibility by how they record dialogue on the set.

21. In automated dialogue replacement, dialogue is recorded or rerecorded in postproduction so there is complete control over the acoustic environment in which the dialogue sits. Any background sound, ambience, or sound effects are added to the dialogue track(s) later.

22. ADR is done in a dialogue recording studio, a relatively dry room with a screen and a microphone.

23. ADR frees picture from sound and gives the director more flexibility and control. On the other hand, it involves re-creating a performance, which is not as natural or as authentic as the real thing.

24. The five elements generally considered to be most important in ADR are pitch, tone, rhythm, emotion, and syn.

25. In scenes calling fo background voices, called walla, loop groups are used.

Read Full Post | Make a Comment ( None so far )Producing Talk And Voice-Overs–Videos

How to Set Up PA Systems : Basic Microphone Placement for PA System Setup

School radio studio tour

How a Radio Station Works : Radio DJ Microphone Placement

Audio-Technica Studio Recording Microphones w/ AVGIANT at NAMM

1. The production chain (in non-music production) generally begins with the talking performer and therefore involves considerations that relate to producing speech.

2. How speech is produced depends on (1) the type of program or production; (2) the medium–radio, TV, film–and, in TV and film, whether the production technique is single– or multicamera; (3) whether it is done in the studio ori n the field; and (4) whether it is live, live-on-tape, or produced for later release.

3. The frequency range of the human voice is not wide compared with that of other instruments. The adult male’s fundamental voicing frequencies are from roughly 80 to 240 Hz; for the adult female, they are from roughly 140 to 500 Hz. Harmonics and overtones carry theses ranges somewhat higher. (Ranges for the singing voice are significantly wider).

4. Speech intelligibilty is at a maximum when levels are about 70 to 90 dB-SP. Certain frequencies, particularly in the midrange, are also more critical to speech intelligibility than others.

5. Acoustical phase refers to the time relationship between two (or more) sound waves at a given point in their cycles. Electrical phase refers to the relative electrical polarity of two signals n the same circuit. When these waves or polarities are in phase–roughly coincident in time–their amplitudes are additive. When these waves or polarities are out of phase–not coincident in time–their amplitudes are reduced.

6. Evaluation of a microphone for speech includes at least four criteria: clarity, presence, richness, and versatility.

7. The closer a microphone is placed to a sound sources, the closer to the audience the sound source is perceived to be and the warmer, denser, bassier, drier, more intimate, and more detailed is the perceived sound.

8. The farther a microphone is placed from a sound source, the farther from the audience the sound source is perceived to be and the more distant, diffused, open, spacious, reverberant, and detached, and the less detailed is the perceived sound.

9. In selecting and positioning a mic, keep excessive sound that is reflected from room surfaces, furniture, and equipment from reaching the mic, or comb filtering can result. Choose a mic and position it to avoid sibilance, plosives, and breath sounds.

10. In monaural sound aural space is one-dimensional–measured in terms of depth–so perspective is near-to-far.

11. In stereo sound aural space is two-dimensional–measured in terms of depth and breadth–so perspectives are near-to-far and side-t0-side.

12. In stereo miking the angle or distance between the two microphones (or microphone capsules) determines side-to-side perspective. The smaller the angle or distance between the mics, the narrower the left-to-right stereo image; the larger the angle or distance, the wider the left-to-right image.

13. In disc jockey, interview, and panel programs, the participants should sound as though they are coming from the front and center of the aural space. With more than one participant, using individual microphones, the loudness levels for the participants must be similar if the sound is to be perceived as coming from the front and center of the aural space.

14. The overall sound of a radio station involves the particular music or talk format, the announcer’s delivery style, the production style of the spot announcements and jingles, and how tightly presented they all are.

15. The techniques used to mike speech for picture in television and film (and to produce sound, in general) may depend on whether the production is broadcast live, or live-on-tape, or is taped/filmed for showing at a later date.

16. In radio microphones can be placed anywhere without regard for appearance so long as the participants are comfortable and the mics do not get in their way. If the radio program is also televised, some care for appearance should be taken. In television, if a mic is in the picture, it should be good-looking and positioned so that it does not obscure the performer;s face. If it is not in the picture, it must be positioned close enough to the performer so that the sound is on-mic.

17. Generally, for optimal sound pickup the recommended placement for a mini-mic is in the area of the performer’s sternum, about 6 to 8 inches below the chin.

18. Hiding a mini-mic under clothing requires that the mic and mic cable are or can be made insensitive to rustling sounds and that the clothing be made of material that is less likely to make those sounds.

19. In television a desk mic is often used as a prop. If the desk mic is live, make sure it does not block the performer’s face, interfere with the performer’s frontal working space, pr pick up studio noises.

20.The handheld mic allows the host to control audience questioning and mic-to-source distance and, like the desk mic, helps generate a closer psychological rapport with the audience.

21. The boom microphone, like the mini-mic hidden under clothing, is used when mics must be out of the picture. Often one boom mic covers more than one performer. To provide adequate sound pickup, and to move the boom at the right time to the right place, the boom operator must anticipate when one performer is about to stop talking and another is to start.

22. Different techniques are used in controlling levels, leakage, and feedback of mic feeds from multiple sound sources: following the three-t0-one rule, moderate limiting or compression noise gating, or using an automatic microphone mixer.

23. If an audience is present, it must be miked to achieve an overall sound blend and to prevent one voice or group of voices from predominating.

24. Increasing audience laugher or applause, or both, by using recorded laugher or applause tracks adds to a program’s spontaneity and excitement.

25. Recording speech begins with good acoustics. Mediocre acoustics can make speech sound boxy, oppressive, lifeless, ringy, or hollow.

26. Recording speech generally involves either the voiceover–recording copy to which other sonic material is added–or dialogue. Voice-over material includes short-form material, such as spot announcements, and long-form material, such as documentaries and audiobooks.

27. Recording a solo performer and a microphone is a considerable challenge: there is no place to hide.

28. Among the things to avoid in recording speech are plosives, sibilance, breathiness, and tongue and lip smacks.

29. Three types of narration are direct, indirect, and contrapuntal.

30. It is often not so much what is said, but how is said that conveys the overall meaning of a message.

31. Voice acting involves “taking the words off the page” and making them believable and memorable.

32. Among the considerations a voice actor comes to grips with in bringing the appropriate delivery to copy are voice quality, message, audience, word values, and character.

33. Studio intercommunication systems are vital in coordinating the functions of the production team. Three types of studio intercom systems are the private line or phone line–PL; studio address–SA: and interruptible foldback–IFB.

Read Full Post | Make a Comment ( None so far )News Journal: Number 26, October 15, 2010: Printing More Money (Quantitative Easing) and The Coming Currency War and Decline In The Purchasing Power of The U.S. Dollar–Robbing The American People–Videos

“True, governments can reduce the rate of interest in the short run. They can issue additional paper money. They can open the way to credit expansion by the banks. They can thus create an artificial boom and the appearance of prosperity. But such a boom is bound to collapse soon or late and to bring about a depression.”

“The gold standard alone makes the determination of moneys purchasing power independent of the ambitions and machinations of governments, of dictators, of political parties, and of pressure groups.”

~Ludwig von Mises

Jim Rogers Currency Wars

“IMF Meeting Stokes Fear of Currency War”

Grant Says Quantitative Easing Is Just Money Printing: Video

Global Currency War Brewing

Is The World On The Verge Of A Currency War?

Daniel Rosen: Currency War

IMF Meeting Stokes Fear of Currency War

Webster Tarpley: “There’s a currency war!”

Heller Says `Very Difficult’ for Fed to Boost Growth: Video

Feldstein Predicts Dollar to Weaken, Boosting Exports: Video

Japan cooperates with US on international currency issues – NHK 101010

US House committee approves China currency bill – NHK 100925

US criticizes China, Japan over currency interventions – NHK 100917

Clyde Prestowitz discusses valuation of Chinese currency

Mar 24 10 Hearing on China’s Exchange Rate Policy, C. Fred Bergsten Opening Statement

Mar 24 10 Hearing on China’s Exchange Rate Policy, Clyde Prestowitz Opening Statement

The Truth About The Economy: Total Collapse

Ron Paul in September 14, 2007

The Federal Reserve System is a banking cartel that benefits the large banks at the expense of the American people.

Cartel economists and so-called experts cannot replace the market by attempting to fix the price of money or the dollar.

Abolish the Federal Reserve System.

Abolish fiat paper currency.

Establish a new United States currency backed by gold.

Milton Friedman on Monetary Policy – 1/3

Milton Friedman on Monetary Policy – 2/3

Milton Friedman on Monetary Policy – 3/3

This is necessary to stop the financing of massive Federal Government deficits by the Federal Reserve that is purchasing U. S. Treasury bills and notes with Federal Reserve Notes by printing money or the monetarization of government debt.

Money printing or quantitative easing decreases the purchasing power of the money supply–debasing of the currency– robbing the American people.

Will the Federal Reserve System and fiat paper money be abolished?

Not any time soon.

The result will first be a longer and deeper recession lasting well into 2013.

In 2013 the Federal Reserve System will be 100 years old.

The Federal Reserves System will celebrate by achieving by then the devaluation of the dollar by 99%.

In other words one dollar in 1913 will be worth 1 cent in 2013.

If this is monetary stability, one wonders what inflation really is.

Time to do away the Federal Reserve System for incompetence.

I do not expect the unemployment rate to fall below 8% for U-3 until 2013 at the earliest.

As unemployment slowly declines in 2011 and 2012, there will be at first a gradual increase in the general price level that will accelerate in 2013.

This will be due the inability of the Federal Reserve to reverse quickly enough its very aggressive expansive monetary policy.

In 2011 and 2012 import prices will rise as the Federal Reserve attempts to devalue the dollar compared with other national currencies in an attempt to expand exports by making them cheaper.

The price of a gallon gasoline in the United States will first rise above $3 in 2011 and $4 in 2012 mainly due to the devaluation of the U.S. dollar.

As Communist China gradually lets the value of its currency rise in value relative to the U.S. dollar, exports from China will rise in price. This means higher prices for goods imported into the U.S. from China.

The decline in the value or purchasing power of the dollar in 2011 and 2012 combined with unemployment rates exceeding 8% will mean further losses for the Democratic Party in 2012 including the Presidency.

The American people are rightfully mad as hell at the ruling class and political elites in Washington D.C.

Power of the Market – How to Cure Inflation 1

Power of the Market – How to Cure Inflation 2

Power of the Market – How to Cure Inflation 3

Ron Paul on the Federal Reserve and Government Deficit Spending

The Gold Standard in Theory and Myth by Joseph Salerno

“The gold standard has one tremendous virtue: the quantity of the money supply, under the gold standard, is independent of the policies of governments and political parties. This is its advantage. It is a form of protection against spendthrift governments.”

“Inflationism, however, is not an isolated phenomenon. It is only one piece in the total framework of politico-economic and socio-philosophical ideas of our time. Just as the sound money policy of gold standard advocates went hand in hand with liberalism, free trade, capitalism and peace, so is inflationism part and parcel of imperialism, militarism, protectionism, statism and socialism.”

~Ludwig von Mises

9. Consolidated Statement of Condition of All Federal Reserve Banks

| Assets, liabilities, and capital | Eliminations from consolidation |

Wednesday Oct 6, 2010 |

Change since | |

|---|---|---|---|---|

| Wednesday Sep 29, 2010 |

Wednesday Oct 7, 2009 |

|||

| Assets | ||||

| Gold certificate account | 11,037 | 0 | 0 | |

| Special drawing rights certificate account | 5,200 | 0 | 0 | |

| Coin | 2,114 | + 3 | + 124 | |

| Securities, repurchase agreements, term auction credit, and other loans |

2,101,199 | + 7,113 | + 216,329 | |

| Securities held outright 1 | 2,051,716 | + 7,403 | + 456,429 | |

| U.S. Treasury securities | 819,072 | + 7,403 | + 49,887 | |

| Bills 2 | 18,423 | 0 | 0 | |

| Notes and bonds, nominal 2 | 752,832 | + 7,390 | + 52,364 | |

| Notes and bonds, inflation-indexed 2 | 42,318 | 0 | – 2,270 | |

| Inflation compensation 3 | 5,499 | + 13 | – 207 | |

| Federal agency debt securities 2 | 154,105 | 0 | + 20,294 | |

| Mortgage-backed securities 4 | 1,078,539 | 0 | + 386,248 | |

| Repurchase agreements 5 | 0 | 0 | 0 | |

| Term auction credit | 0 | 0 | – 178,379 | |

| Other loans | 49,483 | – 290 | – 61,721 | |

| Net portfolio holdings of Commercial Paper Funding Facility LLC 6 |

0 | 0 | – 41,059 | |

| Net portfolio holdings of Maiden Lane LLC 7 | 28,510 | + 40 | + 2,206 | |

| Net portfolio holdings of Maiden Lane II LLC 8 | 15,674 | – 201 | + 1,213 | |

| Net portfolio holdings of Maiden Lane III LLC 9 | 22,782 | – 258 | + 2,616 | |

| Net portfolio holdings of TALF LLC 10 | 601 | 0 | + 601 | |

| Preferred interests in AIA Aurora LLC and ALICO Holdings LLC 11 |

26,057 | + 324 | + 26,057 | |

| Items in process of collection | (84) | 463 | + 98 | + 310 |

| Bank premises | 2,222 | – 7 | + 1 | |

| Central bank liquidity swaps 12 | 61 | 0 | – 49,770 | |

| Other assets 13 | 95,313 | + 2,248 | + 11,389 | |

| Total assets | (84) | 2,311,231 | + 9,358 | + 170,016 |

Note: Components may not sum to totals because of rounding. Footnotes appear at the end of the table. 9. Consolidated Statement of Condition of All Federal Reserve Banks (continued)

| Assets, liabilities, and capital | Eliminations from consolidation |

Wednesday Oct 6, 2010 |

Change since | |

|---|---|---|---|---|

| Wednesday Sep 29, 2010 |

Wednesday Oct 7, 2009 |

|||

| Liabilities | ||||

| Federal Reserve notes, net of F.R. Bank holdings | 918,609 | + 4,849 | + 42,489 | |

| Reverse repurchase agreements 14 | 64,440 | – 2,930 | + 1,540 | |

| Deposits | (0) | 1,253,413 | + 6,593 | + 113,645 |

| Term deposits held by depository institutions | 2,119 | 0 | + 2,119 | |

| Other deposits held by depository institutions | 1,000,014 | + 15,875 | + 33,477 | |

| U.S. Treasury, general account | 49,530 | – 8,299 | + 18,525 | |

| U.S. Treasury, supplementary financing account | 199,962 | + 1 | + 70,006 | |

| Foreign official | 1,345 | – 1,066 | – 540 | |

| Other | (0) | 444 | + 84 | – 9,940 |

| Deferred availability cash items | (84) | 2,598 | + 410 | – 182 |

| Other liabilities and accrued dividends 15 | 15,029 | + 91 | + 6,468 | |

| Total liabilities | (84) | 2,254,089 | + 9,014 | + 163,961 |

| Capital accounts | ||||

| Capital paid in | 26,687 | + 1 | + 1,798 | |

| Surplus | 25,881 | + 6 | + 4,500 | |

| Other capital accounts | 4,575 | + 338 | – 242 | |

| Total capital | 57,142 | + 344 | + 6,055 | |

Note: Components may not sum to totals because of rounding.

1. Includes securities lent to dealers under the overnight and term securities lending facilities; refer to table 1A.

2.Face value of the securities.

3. Compensation that adjusts for the effect of inflation on the original face value of inflation-indexed securities.

11. Refer to table 8.

14. Cash value of agreements, which are collateralized by U.S. Treasury securities, federal agency debt securities, and mortgage-backed securities.

15. Includes the liabilities of Maiden Lane LLC, Maiden Lane II LLC, Maiden Lane III LLC, and TALF LLC to entities other than the Federal Reserve Bank of New York, including liabilities that have recourse only to the portfolio holdings of these LLCs. Refer to table 4 through table 7 and the note on consolidation accompanying table 10.

Minutes of the Federal Open Market Committee September 21, 2010″…At the conclusion of the discussion, the Committee voted to authorize and direct the Federal Reserve Bank of New York, until it was instructed otherwise, to execute transactions in the System Account in accordance with the following domestic policy directive:

“The Federal Open Market Committee seeks monetary and financial conditions that will foster price stability and promote sustainable growth in output. To further its long-run objectives, the Committee seeks conditions in reserve markets consistent with federal funds trading in a range from 0 to 1/4 percent. The Committee directs the Desk to maintain the total face value of domestic securities held in the System Open Market Account at approximately $2 trillion by reinvesting principal payments from agency debt and agency mortgage-backed securities in longer-term Treasury securities. The System Open Market Account Manager and the Secretary will keep the Committee informed of ongoing developments regarding the System’s balance sheet that could affect the attainment over time of the Committee’s objectives of maximum employment and price stability.”

The vote encompassed approval of the statement below to be released at 2:15 p.m.:

“Information received since the Federal Open Market Committee met in August indicates that the pace of recovery in output and employment has slowed in recent months. Household spending is increasing gradually, but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software is rising, though less rapidly than earlier in the year, while investment in nonresidential structures continues to be weak. Employers remain reluctant to add to payrolls. Housing starts are at a depressed level. Bank lending has continued to contract, but at a reduced rate in recent months. The Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability, although the pace of economic recovery is likely to be modest in the near term.Measures of underlying inflation are currently at levels somewhat below those the Committee judges most consistent, over the longer run, with its mandate to promote maximum employment and price stability. With substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to remain subdued for some time before rising to levels the Committee considers consistent with its mandate.The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels for the federal funds rate for an extended period. The Committee also will maintain its existing policy of reinvesting principal payments from its securities holdings.The Committee will continue to monitor the economic outlook and financial developments and is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation, over time, to levels consistent with its mandate.”